In the investment world today, investors are spoiled for choices - and it is no wonder that many find it daunting to decide where to start. Many tend to dabble into “popular stocks” with great amount of coverage, particularly on social media platforms - but often forget that only wide moat stocks are able to provide sustainable returns due to their earnings longevity.

Stocks with a wide moat - tend to have a significant market share in their own industry with little to no alternatives. Such companies are able to withstand price competition, maintain margins and sometimes grow at a staggering rate. Many of them have gone on to deliver impressive returns after a decade or two - such as Visa/Mastercard, Apple, Amazon, Microsoft, Moody's/S&P Global. Most have delivered thousands of percent in returns, especially for investors that kept their eyes on the prize - and focused on owning wide moat stocks.

In this article, we’ll uncover two hidden monopolies that have gone under most investors’ radar, given that everyone is obsessed with names like Tesla, Nvidia and FAANG stocks.

Table Of Contents:

Is BlackRock a Good Investment?

Risk Factor: Is BlackRock a Good Stock to Buy?

Is Verisign a Good Investment?

Risk Factor: Is Verisign a Good Stock to Buy?

1. BlackRock Inc (BLK) Stock

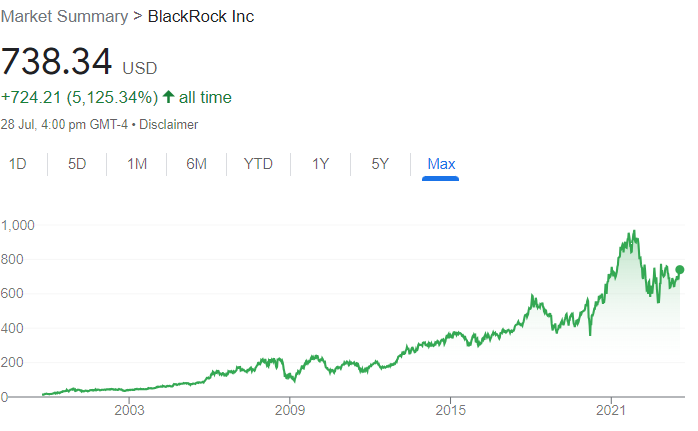

Source: Google Finance

We reckon that many investors have probably heard of BlackRock Inc., but have not studied or looked into them closely before.

Is BlackRock Stock a Good Investment?

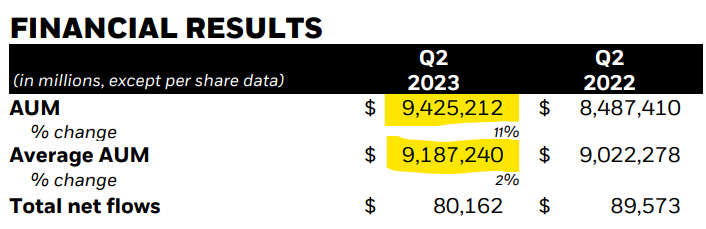

Source: BlackRock Inc. Q2’FY23 Results

Blackrock Inc. is essentially the world’s largest asset manager with more than 9 trillion dollars in Asset-under-Management (AUM). Yes, you’ve read that right. 9 TRILLION freaking dollars. Some investors might be slightly turned off by the number, wondering how much more growth BlackRock can have.

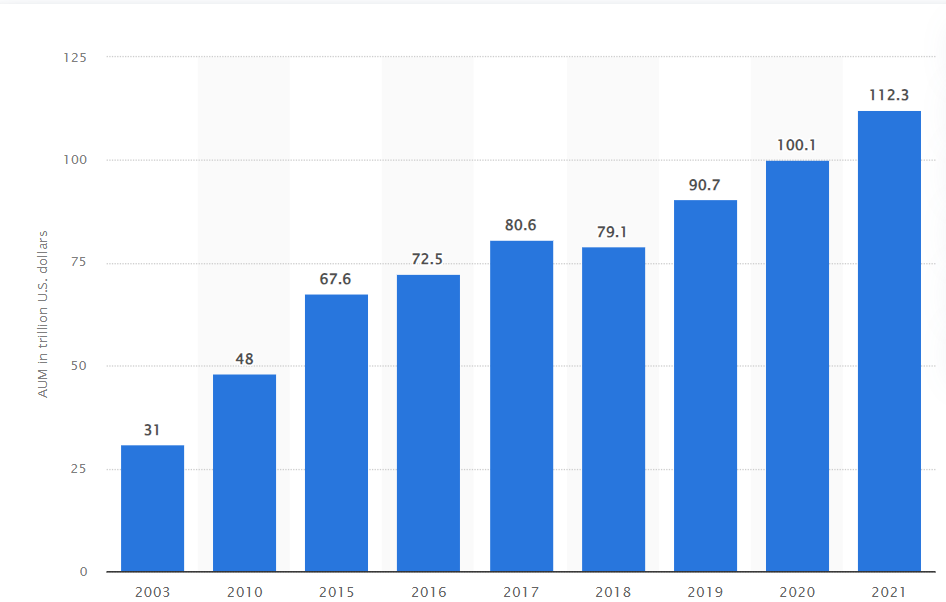

Source: Statista, Value of AUM worldwide in selected years from 2003 to 2021 (in trillion USD)

Funny enough, despite BlackRock being the industry leader, there is still a large runway for growth, and the charming characteristic of investing in a global wealth management firm is their ability to scale infinitely alongside the global economy as more investors accrue more wealth over time.

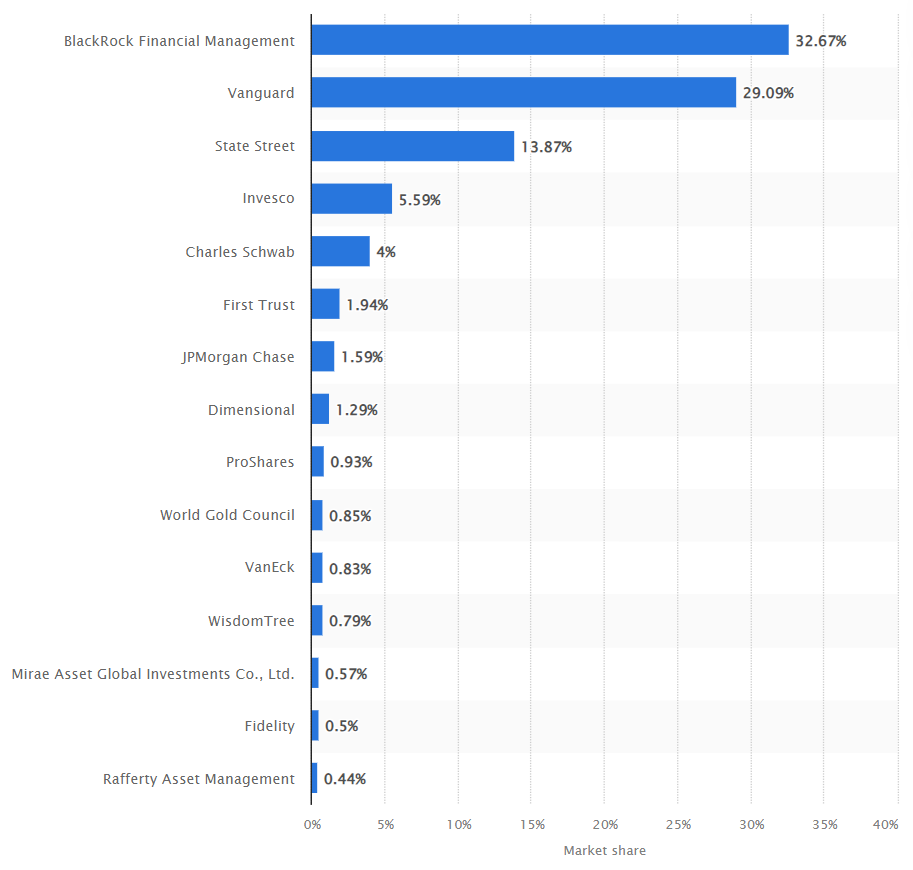

Source: Statista, Market share of largest providers of ETFs in the United States as of July 2023

On a retail level, BlackRock is dominating as the largest provider for exchange-traded funds (ETFs) as they have gained popularity over the years with more people being introduced to the idea of passive investing, while tracking the index.

On the other hand, BlackRock also has a respectable footprint in the institutional wealth management space, which makes up around half (4.5 trillion) of their total AUM.

At the very core, as Laurence Fink, Chairman and CEO of BlackRock, suggested in their recent earnings result, BlackRock is a company that provides a platform-as-a-service strategy to deliver a better investment and technology outcome. They focus on delivering value-added services like solution variety, and technological know-hows such as Aladdin — a portfolio management tool that many clients adopt and leverage on.

According to a 2020 report in the Financial Times, the Aladdin software has been deployed to oversee more than 21.6 trillion worth of assets globally. Vanguard and State Street Global Advisors, who are the largest fund managers following BlackRock, adopt their software for portfolio management too.

Like many successful companies, BlackRock has been ruthless in crushing their competitors. They’ve made several notable acquisitions over the years — one of them back in 2019, where they bought eFront, a French startup that built software with specific money management tools, for $1.3 billion.

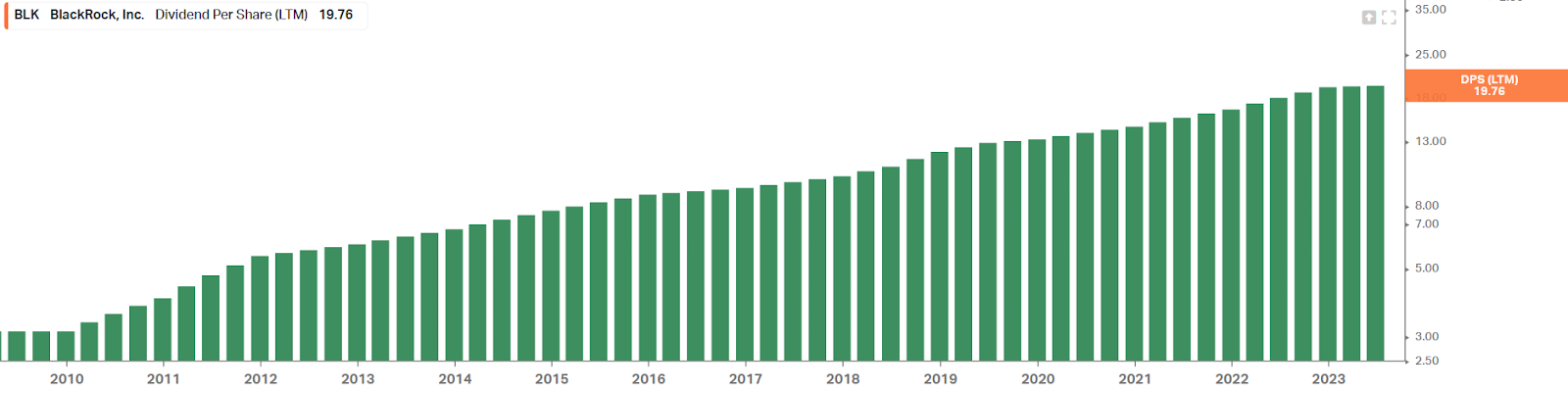

Source: Koyfin

Of course, it doesn’t harm to know that BlackRock has a proven track record of providing strong dividend growth over the last decade or so — further substantiating its market position and earning power.

However, we do have to take into account several potential risk factors.

Risk Factors: Is BlackRock a Good Stock to Buy?

First, no doubt, BlackRock has a strong brand image and market dominant position, but this could potentially be eroded over time, if the management starts to get complacent. The asset management business relies heavily on trust and brand equity, which is both a blessing and a curse. Blessing as it is hard for a newcomer to displace the incumbent, but curse being maintaining the trust and image they’ve built.

Second, there is a certain cyclicality to the wealth management business. As seen in 2022, AUM might be negatively impacted as clients start to draw money out during a bad market (which is counter-intuitive, because you probably want to invest more in a bear market).

Despite that, we believe that BlackRock currently has a rather strong economic moat as a business. Whether it makes a good investment or not will depend on its fundamentals and stock valuation.

2. Verisign, Inc (VRSN) Stock

Source: Google Finance

Unless you are in the IT/web development industry, you’ve likely not heard of this company.

Is Verisign Stock a Good Investment?

At first glance, when you look at the stock’s performance over the last two decades, you might be intrigued by what happened to Verisign in the 2000s.

Long-time investors would recall the dot-com era. Well, Verisign was one of the prominent candidates that suffered greatly from the bubble’s burst.

An important lesson for investors: Even if you’re buying into a company with supposedly strong fundamentals, you must do your independent valuation work to ensure that you do not overpay. In Verisign’s case, investors that were caught in the dot-com bubble only broke even after 20 years (assuming that they bought somewhere near the peak).

That said, we are currently judging Verisign purely from a fundamental perspective, and it passes the criteria of being a strong monopoly in their space.

A quick overview of Verisign’s business; they are essentially the custodian of important digital domains such as .com, .net, .tv, .edu and .gov top-level domains (TLDs).

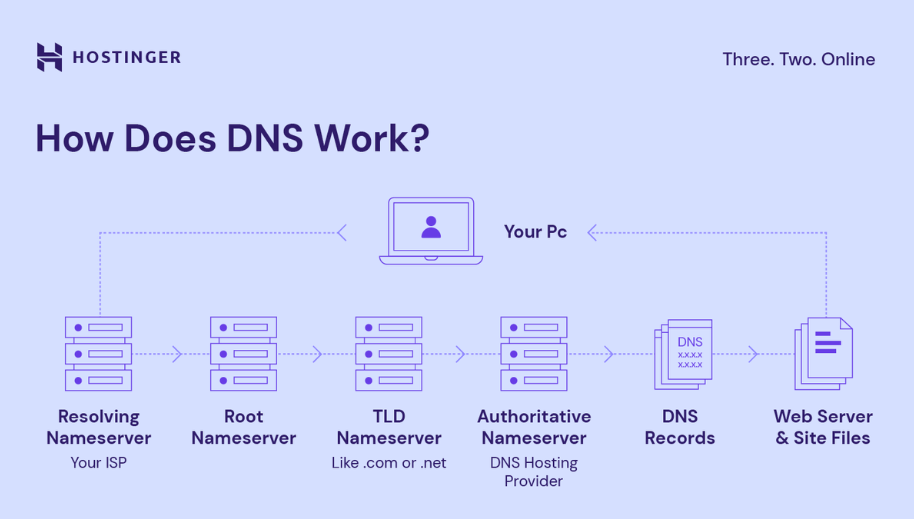

Source: Hostinger

To have a better appreciation of Verisign’s business, you need to roughly understand how the Domain Name System (DNS) works. Long story short, every website you visit has a unique Internet Protocol (IP) address attached to it, which serves as a unique identifier for anyone to access them globally.

The DNS helps translate domain names into these IP addresses so the browsers can load the different resources uploaded on the website, and users need not remember the convoluted IP address.

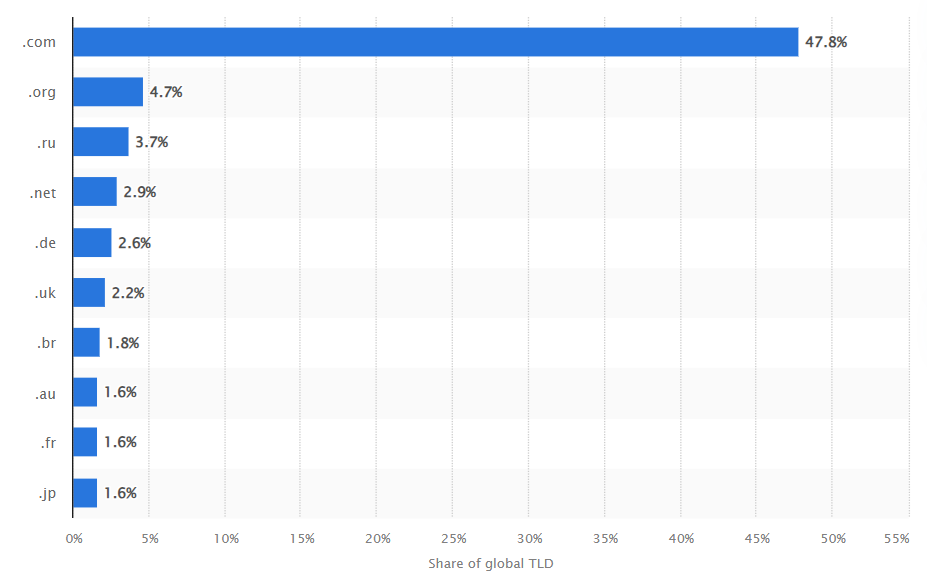

Source: Statista, Most popular top-level domains worldwide as of June 2023

Verisign operates exclusively for websites that end in “.com” and “.net” and if anyone wishes to create a website with the TLD, you will need to pay Verisign an annual fee. Considering the vast market share held by the “.com” domain extension, their moat is as wide as it can be.

The appeal of Verisign as an investment really sits on their inherent subscription-based business model, and the inertia for many existing businesses to switch over to an alternative domain.

On the idea of the subscription model, the retention rate of Verisign clients is astronomically high — typically in the 70 to 80% range. In a recent disclosure by the management team, the highest cancellation rate is usually during the first year of domain ownership. This is intuitive as the goodwill and brand recognition of new business websites might not be as entrenched, so they can afford the switch.

On the flip side, can you imagine if a major company like Google decides to switch from “google.com” to “google.ck” or something along those lines. It would generate so much pushback and inconvenience. Therefore, this suggests that the economic moat of Verisign is largely established as major companies would not risk fooling around with their websites.

Risk Factors: Is Verisign a Good Stock to Buy?

When looking at the highest profile risk factor, as alluded to at the start, Verisign is a “custodian” for these TLDs. ICANN (Internet Corporation for Assigned Names and Numbers) is the one responsible for IP address space allocation and DNS management. In the catastrophic event where ICANN decides to go with another provider to deliver the “.com” and “.net” services, Verisign will probably cease to exist.

That said, the scenario of that happening is close to zero as they usually operate under a “presumptive” right for renewal for continuity.

Another potential threat would be the slow move towards other domain names such as “.ai”, which is picking up in popularity recently. This concern is less meaningful for already established clients that rely heavily on customers memorizing their website domain name, but more so for up-and-rising clients (i.e. growth moving forward).

That said, we do believe that the majority of mindshare still resides with the “.com” and “.net” handles, where arguably, clients may attach a certain premium and legitimacy to it, and thus think twice before taking up alternative handles.

Conclusion

Despite feeling upbeat and optimistic about the future of both BlackRock and Verisign from a business perspective, we believe that investors should only buy stocks when they provide a margin of safety.

If you’re keen to invest in the two companies discussed above and want to discover even more strong potential stock ideas, do check out the Ultimate Investors Playbook where Adam Khoo has done deep-dive analysis of the competitive landscape, financial performance and valuation framework around these stocks.

Till the next time, Keep Winning.

submit your comment