NVIDIA is a strong beneficiary of this crazy rally behind AI stocks over the last three months. We recently shared our perspective on whether NVIDIA is a good stock to buy.

Piercing through the hype, we believe that these are the three key factors an investor should consider before investing into NVIDIA:

Table of Contents:

NVIDIA’s Chip Demand Sustainability

With the explosion of ChatGPT, many companies seem to be jumping on board with honing their “AI capabilities” — whatever that means. As generative AI is brought to the attention of business leaders, there might be a sense of FOMO (fear of missing out) and businesses might be compelled to spend blindly in the near-term, so as to announce to the world that they are at the frontier of their industry.

This causes problems in two folds. Demand and Price.

First, there might be a “pull-forward” effect as more companies are rushing to build their AI infrastructure, thereby artificially boosting the demand for high-end chips in the short term, distorting the actual level of demand for such chips, making projections from this high base flawed.

Second, in this near-term AI rush, companies might be bidding the prices of NVIDIA chips up because of the limited supply, thereby allowing NVIDIA to provide such monstrous revenue guidance for the following quarters. Once demand normalizes, prices might revert and subsequent projections will have to be recalibrated again.

Our skepticism is predicated on both the cyclical nature of the semiconductor industry, and the lack of guidance in spending from upstream (suppliers like TSMC) and downstream (customers like Google, Microsoft, etc.) stakeholders in NVIDIA’s value chain.

We can observe that the semiconductor industry as a whole is currently experiencing a down-cycle where revenues are contracting at an alarming rate.

Assuming that the demand for NVIDIA’s chips is sustainably forecasted, there should be hints of trying to procure and boost production to meet the up-and-rising demand.

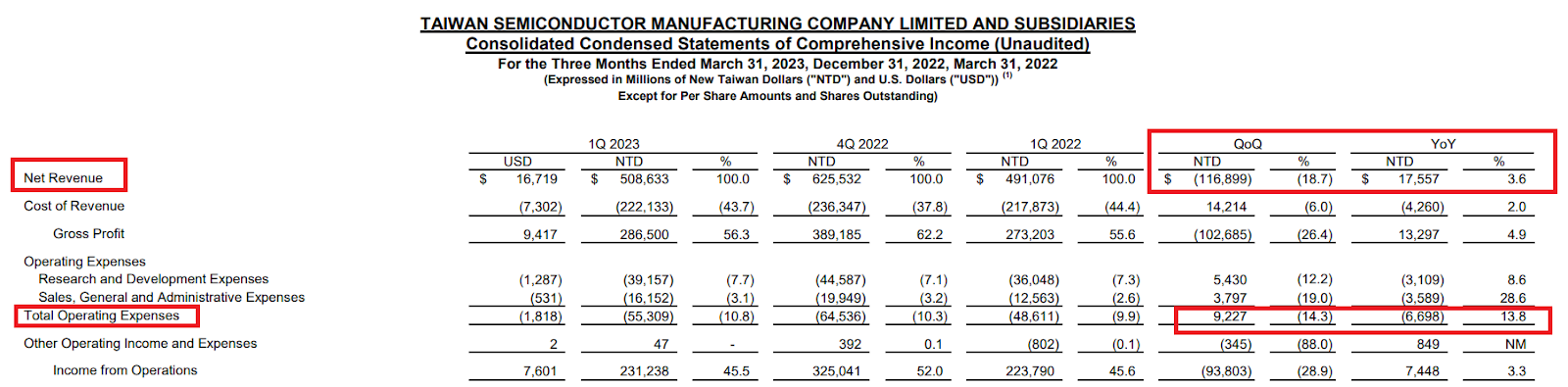

Source: TSMC’s FY23’Q1 Earnings Report

When cross-referenced with Taiwan Semiconductor Manufacturing Company (TSMC), one of NVIDIA’s main suppliers, we don’t see this playing out.

In fact, in TSMC’s latest earnings report, Revenue was -18.7% QoQ while Operating Expense was -14.3% QoQ, showing weak signs of significant output requirements from their customers (with NVIDIA being one of them).

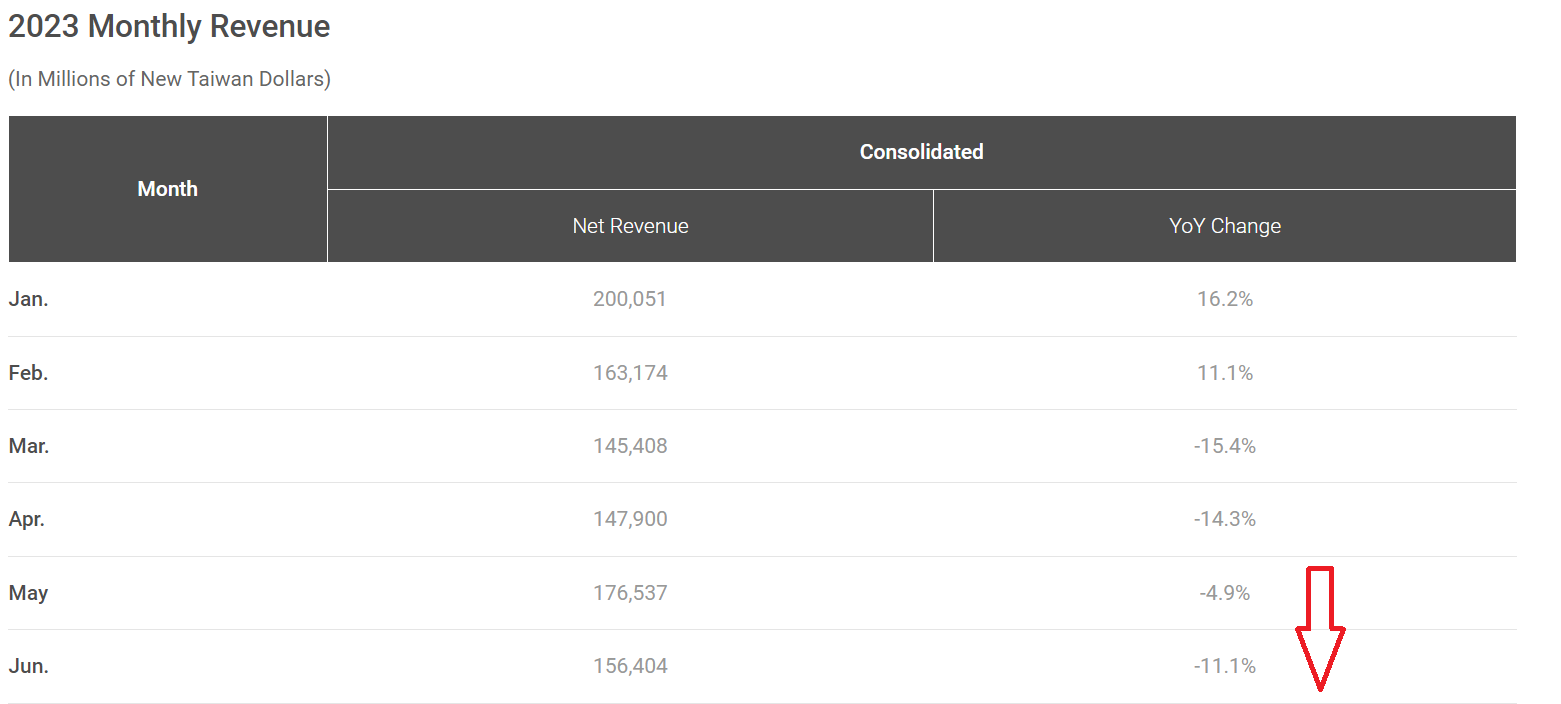

Source: TSMC’s 2023 Monthly Revenue Report

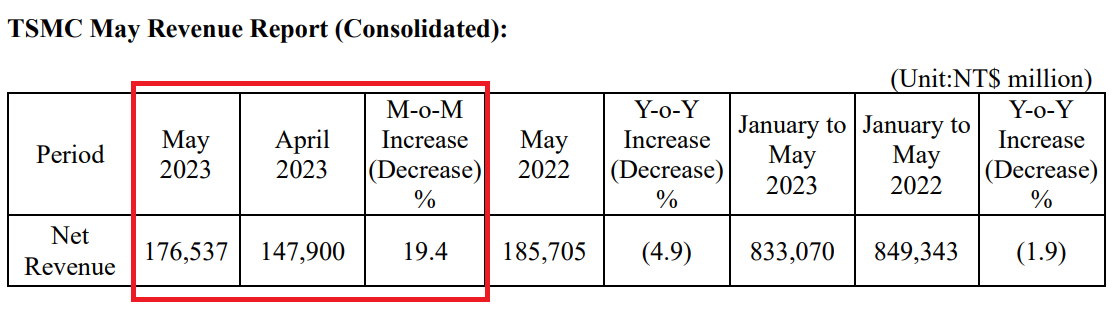

Source: TSMC’s May 2023 Revenue Report

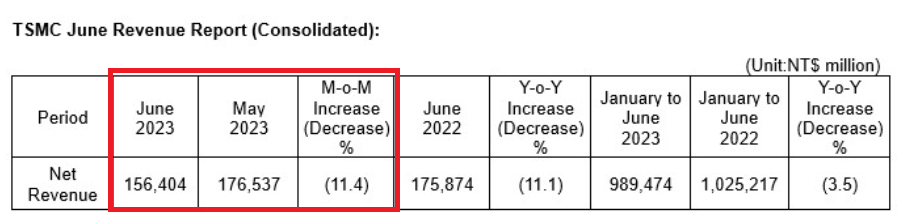

Source: TSMC’s June 2023 Revenue Report

However, do note that there is a significant step-up in chip manufacturing demand as seen from TSMC’s May 2023 revenue disclosure, with a +19.4% MoM increase. This could potentially suggest that NVIDIA’s GPU production demand MIGHT be helping to soften this semiconductor down-cycle (despite still being -4.9% YoY).

On the flip side, when we look at the major enterprise customers of NVIDIA, specifically the Big Tech companies that are involved in the Cloud business, we don’t see a significant uptick in either Operating or Research & Development expenses guidance.

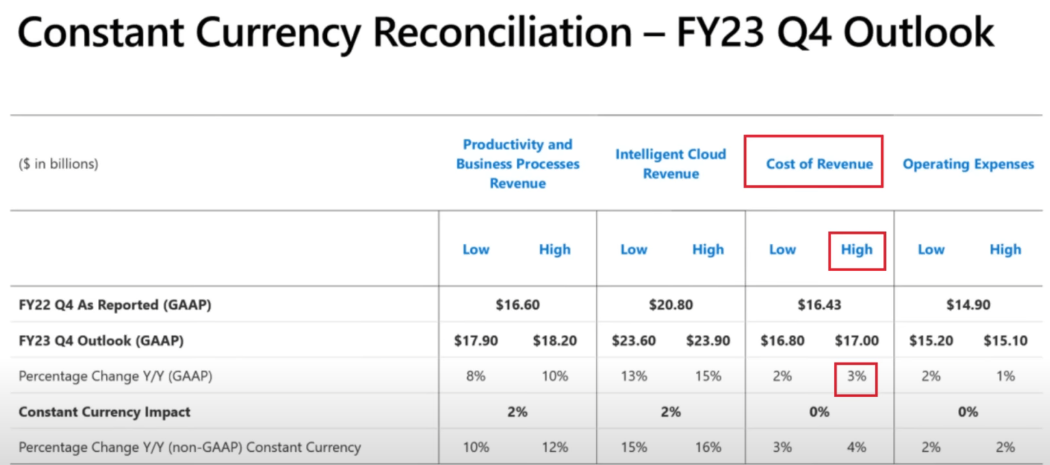

Source: Microsoft FY23’Q4 (June 2023) Outlook

At least for Microsoft, they do not expect to see a significant bump in Cost of Revenue and Operating Expenses from their disclosures.

Google and Amazon on the other hand did not provide such granular breakdown for their Q2 outlook.

Amazon’s Q2 guidance of $127 – 133B in sales and $2 – 5.5B in operating profit, was largely in line with expectations of $130.5B in sales and $4.4B in operating profit.

Source: TechNode

We would acknowledge that there is a surge in demand for NVIDIA’s products in the recent two quarters, from stakeholders like ByteDance, Oracle, etc. However, in order to sustain that $44 billion run rate per year ($11B/quarter guided by NVIDIA), only large companies currently have the capacity to contribute to this revenue flow.

We have no doubt that NVIDIA is able to achieve this US$11 billion revenue target +/- 2%, but this then leads us to wonder if this flow of demand for NVIDIA’s chips is sustainable and meaningful to make any future financial projections.

Competition from Customers

NVIDIA and its customers share a very special relationship. Although many of them are currently reliant on NVIDIA for their high-end chips, many of these large enterprises are constantly innovating to break out of this dependent relationship.

Google, one of NVIDIA’s notable customers, unveiled in 2017 the second generation of their in-house tensor processing unit (TPU), which was crafted for the sole purpose of taking on artificial intelligence (AI) workloads.

Just recently in April 2023, Google claimed that a supercomputer powered by their own latest TPU outperformed a system powered by comparable NVIDIA chips by up to 1.7x.

However, this claim to victory was proven to be short-lived as the comparison was between Google’s latest TPU and NVIDIA’s A100 chip (launched in 2020).

In NVIDIA’s latest reveal of their H100 chip (March 2022), they said that it would be 9x faster for training AI models when compared to the A100, and would be the most power-efficient NVIDIA GPU to date, suggesting that their H100 processor will likely out-compete Google’s effort to the throne.

Elon Musk, CEO of Tesla, was also touting back in 2019 that they will be using Tesla’s custom GPU processor, instead of NVIDIA’s solution — because their custom design “beats them by a huge margin”.

That said, NVIDIA did retort, lamenting that Tesla’s comparison to its GPU was incorrect. For now, Tesla has since turned self-reliant for their chip designing needs.

The larger lesson to take away from this is the nature of NVIDIA’s competitive environment. On top of their main competitors in the chip designing industry (like AMD and Intel), their customers are also joining in the arms race to be self-sufficient — as some might be uncomfortable with the repercussions of NVIDIA’s current near-monopoly status.

NVIDIA’s Chinese Market Restrictions

Given the increasing tension between the Sino-US relationship, the chip industry is poised to be the next battleground. In late 2022, the US government told NVIDIA to stop selling chips in China and Russia in an attempt to slow down China’s efforts in AI research and deployment.

To counter this restriction, NVIDIA introduced the A800 (which operates at 70% speed of the A100 GPUs), while complying with the US export standards that limit the level of processing power NVIDIA can sell. This barely allowed NVIDIA to retain its Chinese demand for chips.

For context, in fiscal 2022, China and Hong Kong accounted for around 31% of NVIDIA’s revenue, and it continues to prove an important market as China deems the high-end semi-con industry to be of strategic importance.

We believe this sort of export ban or restriction will be a recurring theme, so long as the relationship remains unrepaired. Therefore, we expect more volatility ahead as NVIDIA navigates this tricky geopolitical situation.

Furthermore, Jenson Huang (NVIDIA’s founder and CEO) has warned about China’s resolve and determination to build its own advanced semiconductor capabilities amidst these chip restrictions imposed on them unilaterally.

Therefore, the competitiveness of China’s in-house chip designing firms will remain a black box until the day that they turn self-reliant, and NVIDIA’s China demand will be challenged.

Conclusion

Despite the constant iteration of potential pitfalls and risks surrounding NVIDIA today, we are cautiously optimistic about NVIDIA’s future ahead due to its competitive capabilities in the chip designing space.

submit your comment