Singaporeans, you must have heard this by now. The Central Provident Fund (CPF) Special Account will be closed for members aged 55 and above – as announced at the Singapore Budget 2024. This created quite a hoo-ha, especially amongst folks in their 40s and 50s who are near retirement and some might be worried about how this would affect their nest egg.

Table Of Contents:

How Does the CPF Special Account Closure Affect Me?

Closure of CPF Special Account: Best Investment Alternatives?

Learn to Invest in Winning Stocks to Multiply your Returns Today

How Does the CPF Special Account Closure Affect Me?

The “CPF Special Account Shielding” Hack

Before this announcement, CPF members were able to exploit a “loophole”, where they could “shield” or prevent monies in their SA from being transferred to their Retirement Account (RA). They do so by investing the money in excess of the first S$40,000 into vehicles like Treasury bills, Singapore Bonds, and lower-risk unit trusts or bond funds just before turning 55.

After turning 55, and their RA account is formed, CPF will extract the $40,000 from the SA, and the remaining from the Ordinary Account (OA) to serve as their retirement funds. Those who did the “shielding” hack could subsequently sell their investment and move the proceeds back to their SA after their 55th birthday to enjoy the minimum 4% risk-free, guaranteed interest. PLUS they enjoyed the option to withdraw at any time they wanted to, as long as they had their cohort’s Full Retirement Sum (FRS) fulfilled.

With this CPFSA closure, it means that members are no longer able to enjoy the minimum 4% risk-free and liquid “savings account”, which easily beats any other offers in the market today. From 2025 on, all excess funds will be transferred to the OA instead – that earns a much lower 2.5% interest.

The 1M65 Movement

Before this CPFSA closure announcement, there were popular strategies online like the 1M65 Movement, which outlines the strategy of how a couple can achieve SGD 1 million in their combined CPF accounts by age 65.

The 1M65 Movement is really just a simple formula of compounding. If a young couple by the age of 30 is able to amass $130,000 each in their OA + SA accounts, they can decide to transfer all of their OA balance into SA to earn that 4% p.a. interest.

Applying the formula, $130,000 x (1.04)^35 x 2 = $1,025,983.

Voilà, that’s where you get your 1 million by 65 years old.

However, in light of the CPF Special Account closure, members will no longer be able to compound their SA monies freely while still keeping its liquidity. They are met with one of two options:

- If they want to cash out their CPF monies in the future (anything above the FRS), they will need to accept the lower interest rate of 2.5% – as it is being transferred to the OA.

- Or, if they still want to take advantage of the 4%, it will lose its liquidity as it will be fed into the RA instead, coming back to them in the forms of life-long monthly payments after retirement age.

CPF Special Account Closure: The Real Opportunity Cost in Dollars

You might be wondering what is the actual dollar impact to someone nearing retirement, if he/she still wishes to keep the liquidity of their SA funds.

Let’s be clear – this SA closure will only affect those that are above the FRS figure ($205,800 as of 2024) at 55 years old. If the member has anything below that, they will not be able to withdraw (any excess) either way.

The simple calculation for the opportunity cost in that ten-year period would be

(1.0408 - 0.025)^10 = 1.0158^10 = 16.97%. If we were to delay it until 70 years old before withdrawing instead, that would be (1.0158^15) = 26.5%.

The dollar impact would be dependent on how much extra the member has above the FRS. For every $100K at age 55, the opportunity cost derived from the closure of the SA, switching over to the OA, is a ~$17,000 loss in potential returns over a ten-year period.

This is a devastating blow, especially to those who opted for a voluntary transfer from OA to SA, and those who had diligently topped up cash to their CPF SA, hoping to ride on the compounding effect while keeping the pool of money liquid for retirement.

Given this huge loss in potential, it now makes sense to park any excess funds into better-performing vehicles, rather than topping up into the CPF. In the next section, we explore the best investment alternatives for Singaporeans who wish to grow their retirement savings.

Closure of CPF Special Account: Best Investment Alternatives

Given the CPFSA closure at age 55, many “young” seniors (or soon to be) are probably wondering about the next best alternatives to invest their excess funds.

For starters, most will probably look to beat the performance of 2.5% risk-free, which is offered by the CPF-OA. At least in the current high rate environment – there are many financial instruments in the market that can deliver better returns through low-risk vehicles.

Note: The following performance figures represent the vehicle’s average return over a given time period. Rates of returns are subject to change depending on market conditions.

Singapore Treasury Bill (T-Bill): 3.74% over Six Months

Source: Monetary Authority of Singapore website

An example would be the 6-month T-bill issued by the Singapore government, which sits at a yield of 3.74% at the time of writing. The biggest benefit? It’s relatively liquid with a short lock-in period of only six months and offers a respectable yield, while having low counterparty risk (which is the Singapore government).

The downside? The reinvestment risk due to the short-term nature of the T-bill. Singapore is an interest-rate taker – which means that we follow the rates of the global market (specifically the US Federal Reserves). 3.74% is a decent yield, but no one knows how long it will last.

Considering that the US Fed has intentions of lowering rates in the near future, the Singapore T-bill yield is not expected to stay at such a high rate for long, and investors will have to bear the consequences of reinvestment risk – six months later, how are you going to allocate the capital?

Singapore Savings Bond: 3.04% over Ten Years

Source: Monetary Authority of Singapore website

To combat the ultra short-term nature of T-bills, the Singapore government offers an alternative - a bond that gives an average return of 3.04% p.a. (over a tenure of ten years).

The good thing? It’s one of the safest alternatives in the market, as it is backed by the Singapore government. There is no lock-in period – and even if you were to “redeem” it early before the bond matures, you’ll receive the interest on a prorated basis.

The bad thing? Although 3.04% sounds like a good deal, it is probably not going to help you compound your money fast enough for your retirement. We just saw Singapore’s headline inflation averaging 4.8% in 2023, and the interest from the bond couldn’t even keep up.

On a similar note, after ten years, there is reinvestment risk involved as well, especially if we return back to low rate environments, and not too long ago (in 2020) SSBs were only delivering a 1.63% yield over ten years.

Bank Deposit Rates: 7.8% p.a. ?!

Source: UOB One Account

Given the high rate environment, some banks like the UOB One Account seek to deliver a high interest rate on your deposits – yet still allowing the customer to keep their funds liquid.

Source: UOB One Account Interest rate tier before 1 May 2024

Essentially, they’ll require you to jump through some hoops (such as minimum spending criteria, and the crediting of your salary via GIRO) – and you’ll enjoy an effective interest rate (EIR) of 5% on your first $100,000 banked with UOB.

Source: UOB One Account Interest rate tier after 1 May 2024

The downside? You’re at the whim of the banks – and they could change the mechanism or even the rates as and when they wish to. We’ve just gotten news that with effect from 1 May 2024, UOB One has decided to reduce the effective interest rate to 4% on the first $150,000 instead of the usual 5% on the first $100,000.

Clearly, this is not a reliable and sustainable way of building your wealth, let alone retirement.

US-based Index Fund (like the S&P 500): Averages 7-10% p.a. over the long-term

How to 2.45x your Twenty-Year Returns by Investing in the US Market

In order for you to build sustainable, long-term wealth – you’ll need a vehicle that is able to provide you with decent returns over a long period of time, and investing is a proven way to do so.

Especially for beginners, investing might be a very daunting task. However, when you look at conventional literature, a US broad-based index fund (like the S&P 500) has historically returned a range between 7 to 10% annually, over a period of 10 to 15 years.

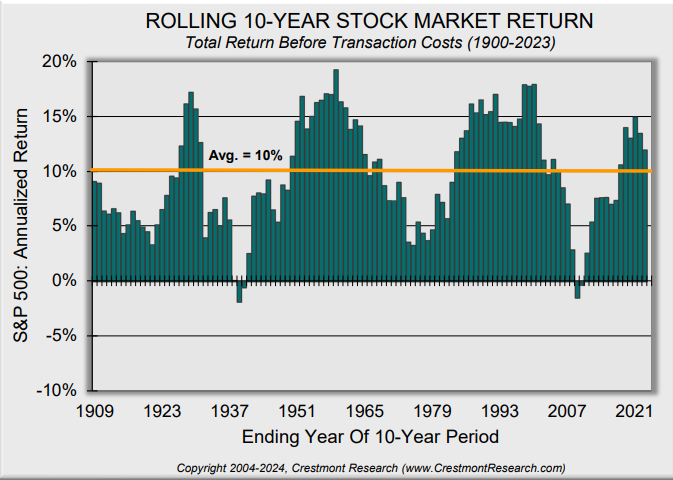

As we can observe, since the 1900s – the S&P 500 has on average returned roughly 10% p.a. That’s 123 years worth of data!

Imagine you’re planning for your retirement at age 45, and you have 20 more years before your ideal retirement age. Let’s do the math (on a base capital of $100,000), comparing between relying on your CPF via the voluntary top-up option versus investing into the US Index.

In CPF (10 years in the SA, subsequent 10 years in the OA (after you turn 55 years old));

$100,000 * (1.04)^10 * (1.025)^10 = $189,483

Versus the US Stock market compounding at 8% (estimated);

$100,000 * (1.08)^20 = $466,095

That’s a 146% difference!

Investing in the US Market as a Relatively Safe Alternative

Those new to investing would have the inevitable concern about how safe an ETF like the S&P 500 really is, compared to putting it into the CPF. Well, it might actually be safer than you think.

For one, the S&P 500 has been a tried and tested way for compounding wealth steadily, over the last century.

Second, this chart says it all.

The longer your time horizon, the lower the risk of investing in the US stock market would be. If we zoom out from 1872 to 2023, and look at every 20-year period (of how the S&P 500 performs), the US stock market has never declined over any 20-year period.

Learn to Invest in Winning Stocks to Multiply your Returns Today

The closer you are to retirement, the shorter the runway is for you to grow and compound your wealth, and that’s the tradeoff everyone is faced with. It’s time to start looking at alternatives that can bring you better returns while keeping the risk relatively low. Instead of being at the mercy of policy changes, we can take charge of our own retirement lifestyle by learning how to invest today.

On top of investing in US ETFs, you can supercharge your returns by learning to invest in the top 1% of the companies in the world. Using the Piranha Profits Value Momentum Investing™ method, it’s possible for investors to achieve double-digit average annual returns.

Want to learn how to grow your money 2X faster and fast-track your retirement? Click here to download our US stock investing guide now.

submit your comment