AI is no longer a niche theme. Most investors are already familiar with the major players, the terminology, and the broad direction the technology is heading. However, what matters in 2026 might not be about which company can demonstrate the most advanced model, but which ones are positioned to make AI deployable and useful at scale. That includes the hardware, infrastructure, and platforms that allow AI systems to operate reliably across industries.

Let’s start with the obvious names that help establish the foundation.

The Backbone of the AI Economy Nvidia(NVDA) stock

While headlines fixate on which company has the best chatbot, Nvidia sits underneath the AI stack. Data centers, large language models, enterprise AI workloads, robotics, and increasingly autonomous driving systems significantly rely on Nvidia’s hardware and software.

Nvidia is still, first and foremost, a compute company. The bulk of its revenue continues to come from selling high-performance GPUs and systems to hyperscalers and enterprise customers training and running large AI models. That chip-centric business funds everything else. But it is no longer the whole story. Nvidia’s DRIVE platform also has evolved into an operating layer for autonomous vehicles, spanning simulation, training, and in-vehicle inference. Extending that same approach beyond cars, Nvidia unveiled open Physical AI models and development tools at CES 2026, enabling robots to perceive, reason, and act in real-world environments.

Despite its size, Nvidia is still seeing powerful demand driven by AI infrastructure buildouts and ongoing platform expansion. Analysts project roughly 30% annual growth over the next few years, with growth in the high-20% range potentially continuing beyond that, assuming solid execution and supportive market conditions.

StockOracle™ valuation chart of Nvidia (NVDA) 18th January 2026

StockOracle™ valuation chart of Nvidia (NVDA) 18th January 2026

Still, the valuation debate is where things get a little uncomfortable. Nvidia continues to screen closer to intrinsic value estimates than many assume. While NVDA may appear expensive on a price chart, the impression softens when viewed through long-term cash flow frameworks. Across valuation models such as DCF-20, DNI-20, and OracleValue™, the stock price is closer to fair value than excess, implying conservative assumptions.

The AI Giant Nobody Is Talking About (Enough) - Amazon (AMZN) stock

If Nvidia represents the physical layer of AI, Amazon (AMZN) represents the layer that makes AI practical.

While investors spent the last cycle piling into flashy AI hardware and software names, Amazon quietly consolidated. The stock lagged.. And that is exactly why it matters now.

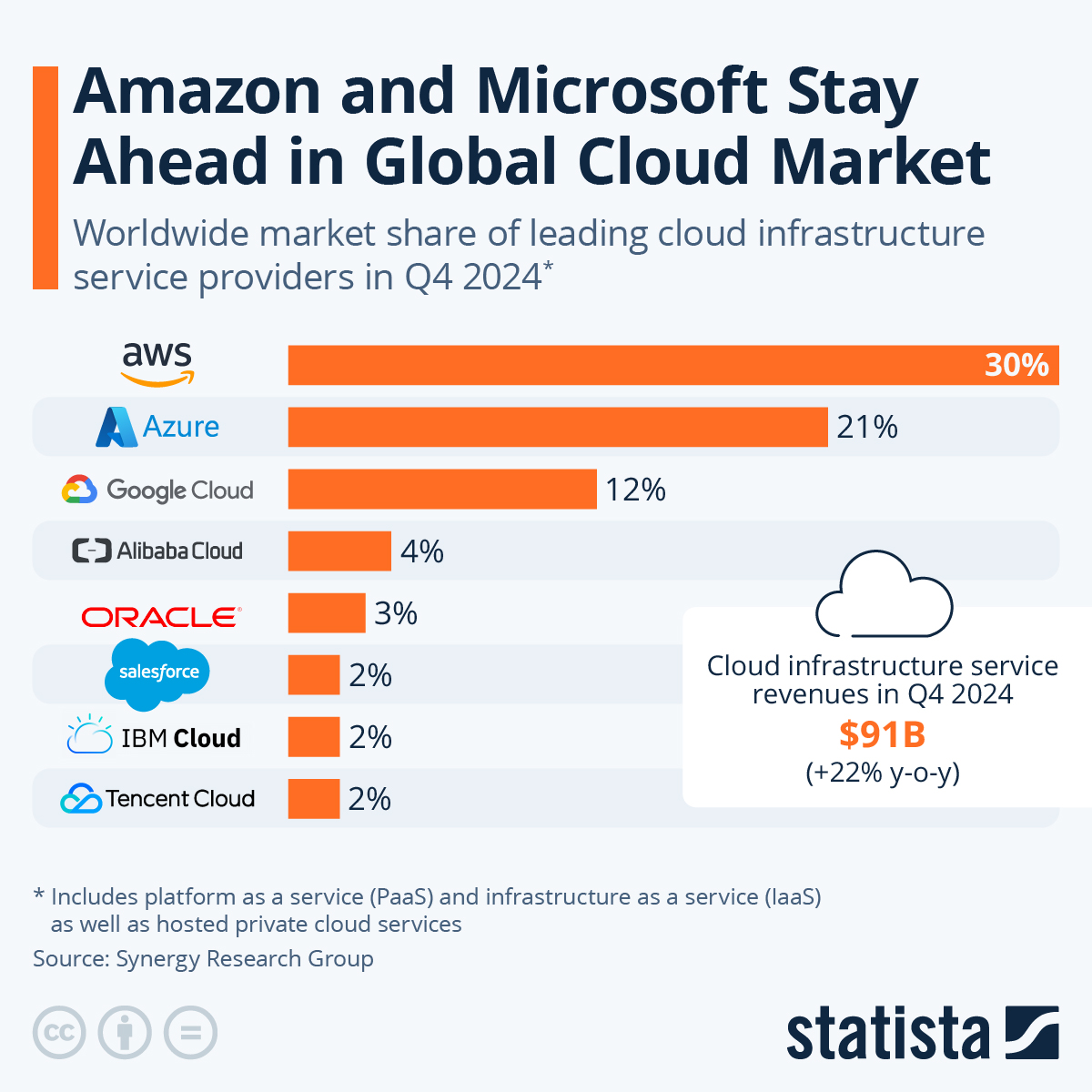

Source : https://cdn.statcdn.com/Infographic/images/normal/18819.jpeg

Source : https://cdn.statcdn.com/Infographic/images/normal/18819.jpeg

Amazon is not solely an e-commerce business. It operates one of the world’s largest hyperscale cloud platforms through AWS, which holds roughly 29% of the global cloud infrastructure market, ahead of competitors such as Microsoft Azure, Google Cloud, and Alibaba Cloud.

AWS plays a central role in enterprise AI deployment, providing the compute, storage, and networking layers required to run large-scale AI workloads. As AI investment moves from experimentation toward sustained production use, the limiting factor increasingly becomes infrastructure capacity and reliability rather than model performance. In that environment, cloud platforms function as the operating backbone rather than optional tools. This positioning places Amazon at the intersection of cloud growth and long-term AI adoption trends.

History offers a useful analogy. In previous tech cycles, the early winners were often replaced by quieter, more durable leaders once the market matured. Many believe Amazon is setting up to be the next version of that pattern. The “boring” stock that potentially isn’t boring anymore.

StockOracle™ AWS’s Value by business segment chart of Amazon (AMZN) 18th January 2026

StockOracle™ AWS’s Value by business segment chart of Amazon (AMZN) 18th January 2026

In 2026, when AI workloads become less about novelty and more about reliability. Amazon is positioned to play a significant role as AI workloads mature and infrastructure reliability becomes more critical.

Enterprise Software Companies Navigating AI Disruption: Salesforce (CRM) Stock and ServiceNow (NOW) Stock

While AI optimism surged, enterprise software stocks like Salesforce (CRM) and ServiceNow (NOW) were punished. Hard. Down almost 40% at peak, written off as victims of AI automation.

The narrative was simple: if AI replaces humans, who needs human-seat-based software?

Chart Powered by TradingView

Instead of being disrupted, these companies are adapting faster than most investors realize. Both are shifting away from per-seat pricing toward outcome-based and agent-driven models. Salesforce’s Agentforce charges based on actions performed by AI agents, not headcount. ServiceNow is building an “agentic fabric” that layers AI capabilities into its platform in ways competitors cannot easily replicate.

Positioning themselves as core platforms for automation and workflow orchestration. Both demonstrate financial resilience, with Salesforce supported by strong free cash flow and accelerating AI-led ARR, and ServiceNow by durable subscription growth and high renewal rates. However, Salesforce faces growing pressure from AI-native and lower-cost competitors, while ServiceNow’s strong execution is tempered by valuation sensitivity.

Other Honorable Mentions: The Quiet POWER Play Behind AI

One final angle investors should not ignore is energy. AI runs on power and global data-center electricity is projected to double by 2030.

Independent power producers (IPPs) like Vistra (VST) and Constellation Energy (CEG) are seeing explosive demand driven by the rapid expansion of AI data centers. Their advantage lies in operating within unregulated power markets and owning nuclear assets that can deliver constant, 24/7 baseload electricity, something AI workloads cannot function without. Hyperscalers are willing to pay premium prices to secure this supply.

However, both stocks are trading at stretched valuations, have weak competitive moats, and lack a long track record of stable cash flows. As a result, the sector carries uneven defenses and higher execution risk, making the selection of individual winners far from straightforward.

This article is for educational purposes only and does not constitute financial advice. The companies discussed are used as examples to explain market trends. Historical data and projections are illustrative and not indicative of future performance. Always conduct your own research or consult a licensed financial adviser before making investment decisions.

{kind=link}

submit your comment