Given the phenomenal run-up of seven of the most prominent tech companies in the world today, many investors are wondering which of these are the best tech stocks to buy now… or is this just another bubble waiting to be popped?

We will explore the current state of The Magnificent 7 and try to make sense of their valuations, risk-reward, and whether they are still a buy today.

Table Of Contents:

Is Apple (AAPL) a Good Stock to Buy Today?

Is Amazon (AMZN) a Good Stock to Buy Today?

Is Microsoft (MSFT) a Good Stock to Buy Today?

Is Alphabet (GOOGL) a Good Stock to Buy Today? [NEW!]

Is Meta Platforms (Meta) a Good Stock to Buy Today? [NEW!]

Is Apple (AAPL) a Good Stock to Buy Today?

From a business fundamentals standpoint, there really isn’t much to complain about. The strength and quality of the Apple brand remain as strong as ever; long-term users in the Apple ecosystem probably have no intentions of switching out, and they continue to print a great deal of cash flow which is largely accrual to shareholders via massive share buybacks.

Source: Macrotrends

However, over the last week or so, there have been renewed concerns around the relationship between China and Apple, where China is reportedly banning officials and state employees from using iPhones. From preliminary calculations, a few analysts have argued that the ban is way overblown as the restrictions would work out to be less than ~500K iPhones out of the roughly 45 million handsets that are expected to be sold in China over the next 12 months. This figure comes out to around 1.1% of Apple’s expected revenue from their Greater China segment. In Apple’s latest quarterly report, China makes up 17.6% of their revenue contribution — so that means a 1.1% on a 17.6% revenue pie — suggesting that it will have a 0.2% impact on overall revenue.

The Chinese ministry has since clarified that “they have not issued laws and regulations to ban the purchase of Apple or foreign brands’ phones”, and that they are instead cracking down on security incidents involving Apple mobile phones (or any phones for that matter), and Bloomberg’s report of China’s ban on iPhones were unfounded.

That being said, we think that the larger “problem” has surfaced to the top over the last two weeks as investors are scrutinizing the symbiotic relationship between Apple and China. On top of demand, Apple’s entire supply chain is rooted in China’s home ground with very little headspace for manoeuver — this reliance was very much reflected during the Covid crisis just three years back.

Apple’s response to this? Diversify, Diversify, Diversify. They are moving production elsewhere bit by bit, but let’s be realistic. Many of such investments and re-configuring of supply chains take time, and sometimes many years. Apple’s dependency on China will not vanish within a few months – prospective and even current investors will have to get comfortable with this foreseeable future of a tit for tat bickering between China and the US.

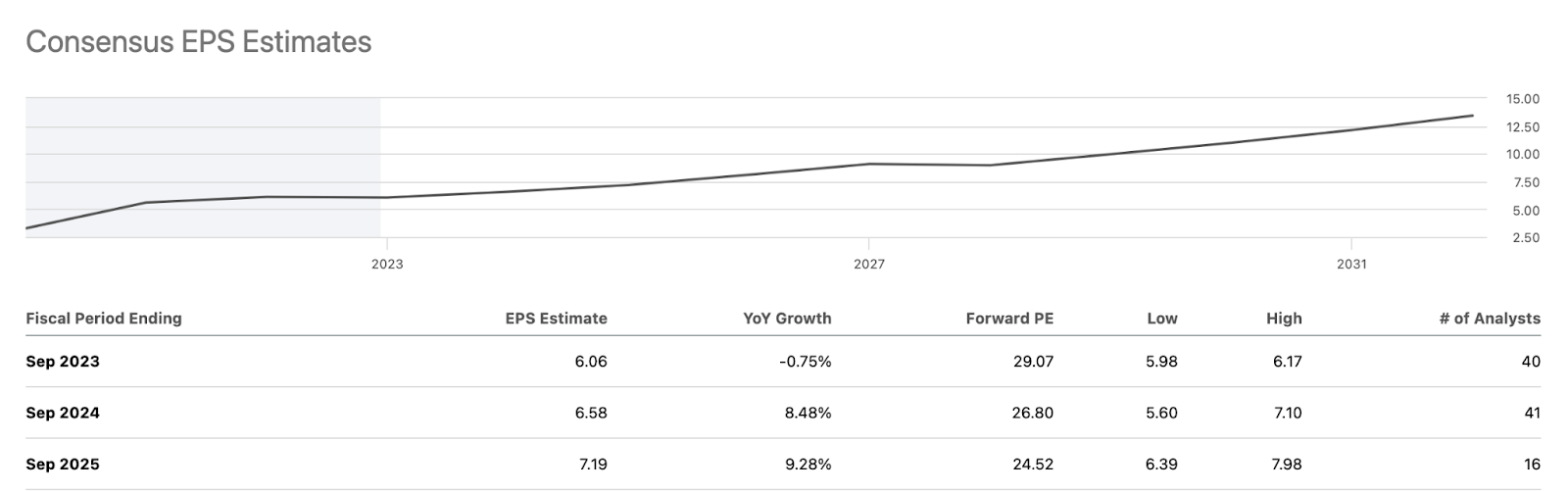

Source: SeekingAlpha Apple’s EPS Estimates

On the valuation front, analysts are expecting Apple’s earnings to not deliver much growth in the coming quarter, but hopefully re-accelerate back to the high-single-digits in 2024 and 2025. Intuitively, being the largest company in the world by market capitalization, Apple has hit a certain level of saturation.

Even with lower growth rates, the market is tagging Apple with a forward PE of 29x, signaling to us that many investors are willing to pay a premium valuation for it.

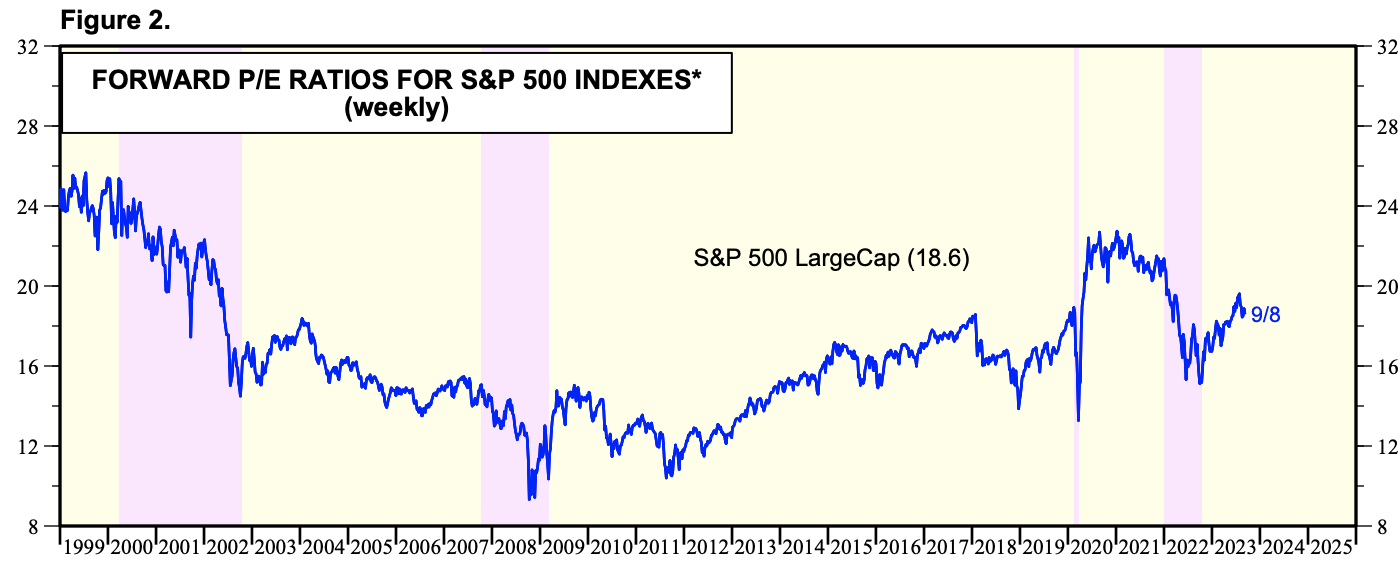

Source: Yardeni Research

The forward PE of the S&P 500 LargeCap sits at around 18.6x. Apple is clearly of better quality than the average S&P 500 company, but I’m not so sure if I’ll call it a “great bargain” now. I do think Apple’s valuation today has already priced in a fair bit of expectations, and would probably hope for a greater margin of safety before entering into the stock.

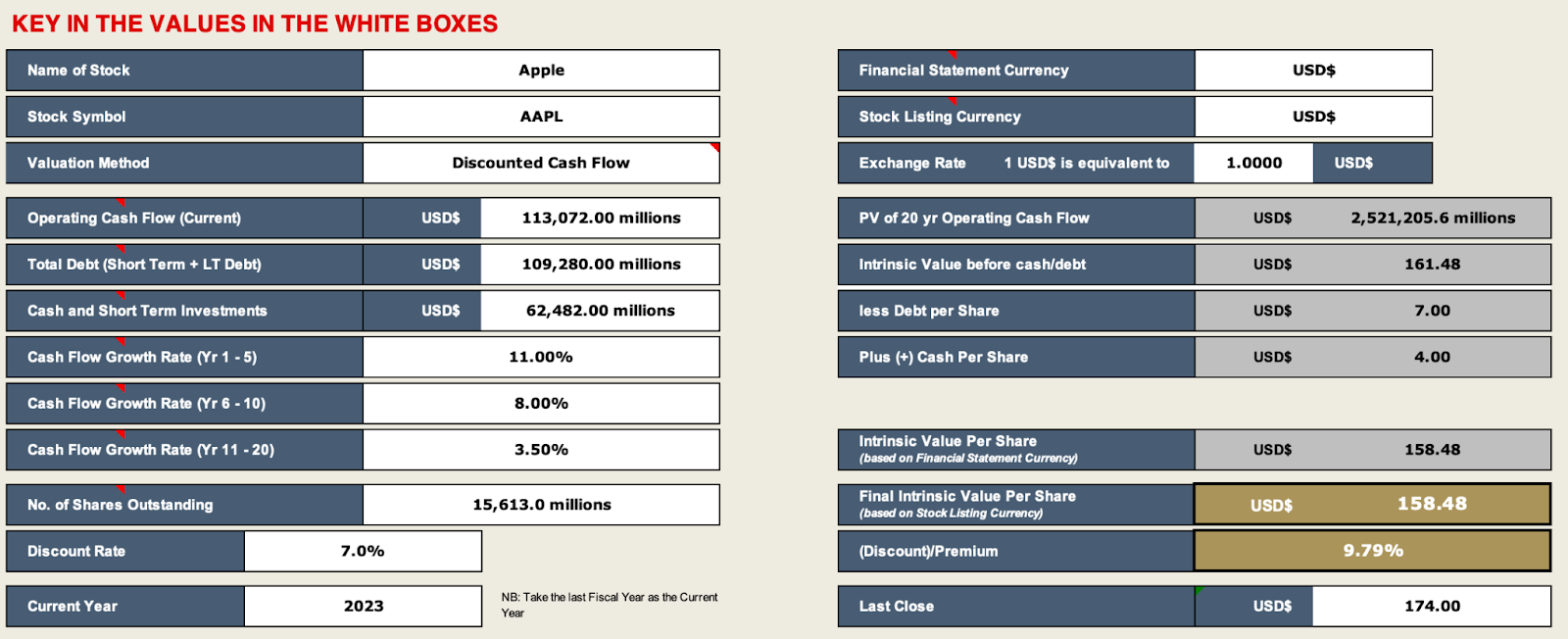

Source: Piranha Profits’ proprietary investing tool — the True Value Finder™

Based on our calculations, the intrinsic value of AAPL stock is right around $158 as of the date of this writing. Comparing it to the close of $174 per share, it is around 10% above the IV. We don’t find Apple egregiously overpriced today but will wait for better prices before adding so as to ensure that we have a greater margin of safety.

Is Amazon (AMZN) a Good Stock to Buy Today?

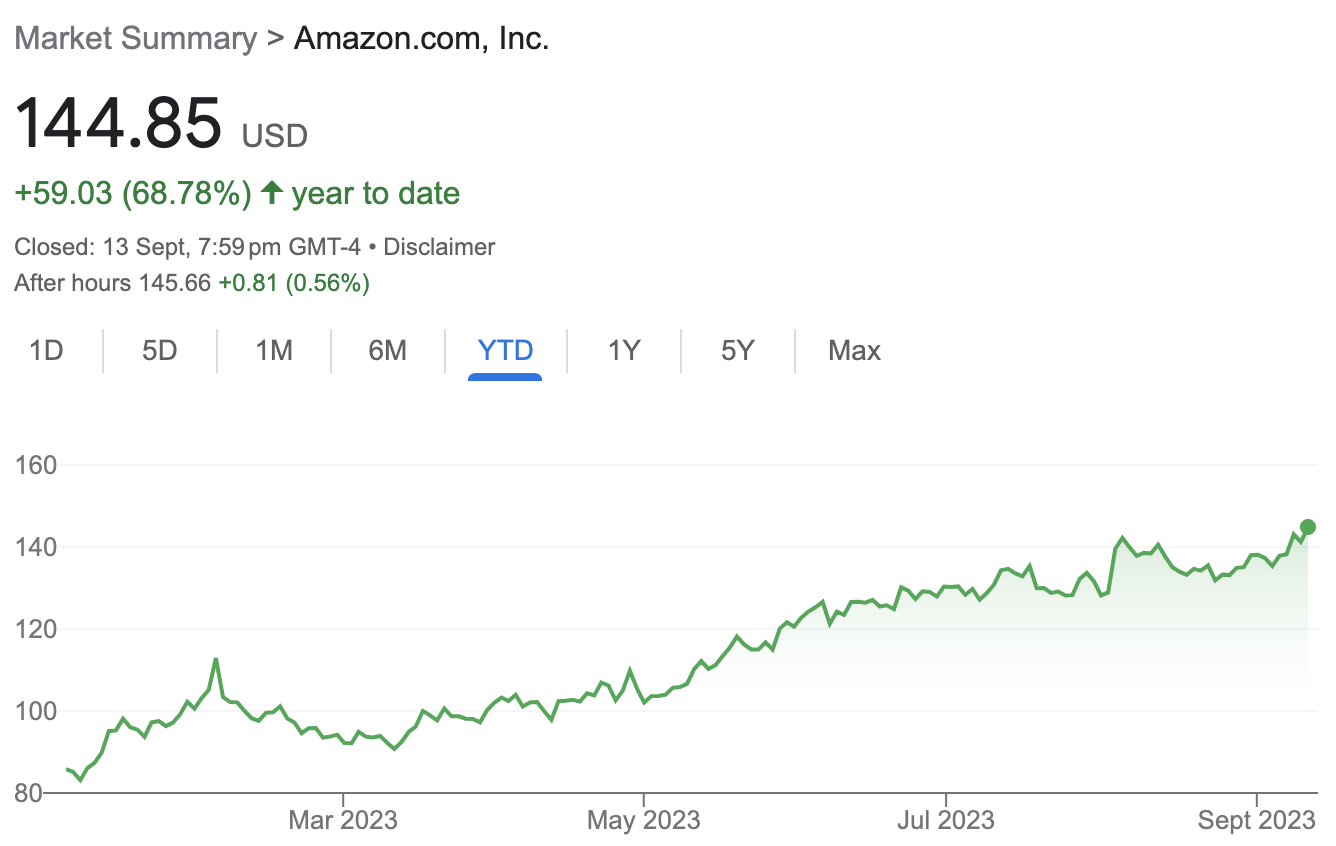

Source: Google Finance

Moving on to Amazon, they have been on a steady uptrend, experiencing a more than 60% appreciation on a YTD basis. Fundamentally, we can observe that the business is turning around the corner and coming out gradually from its investment cycle just some quarters ago.

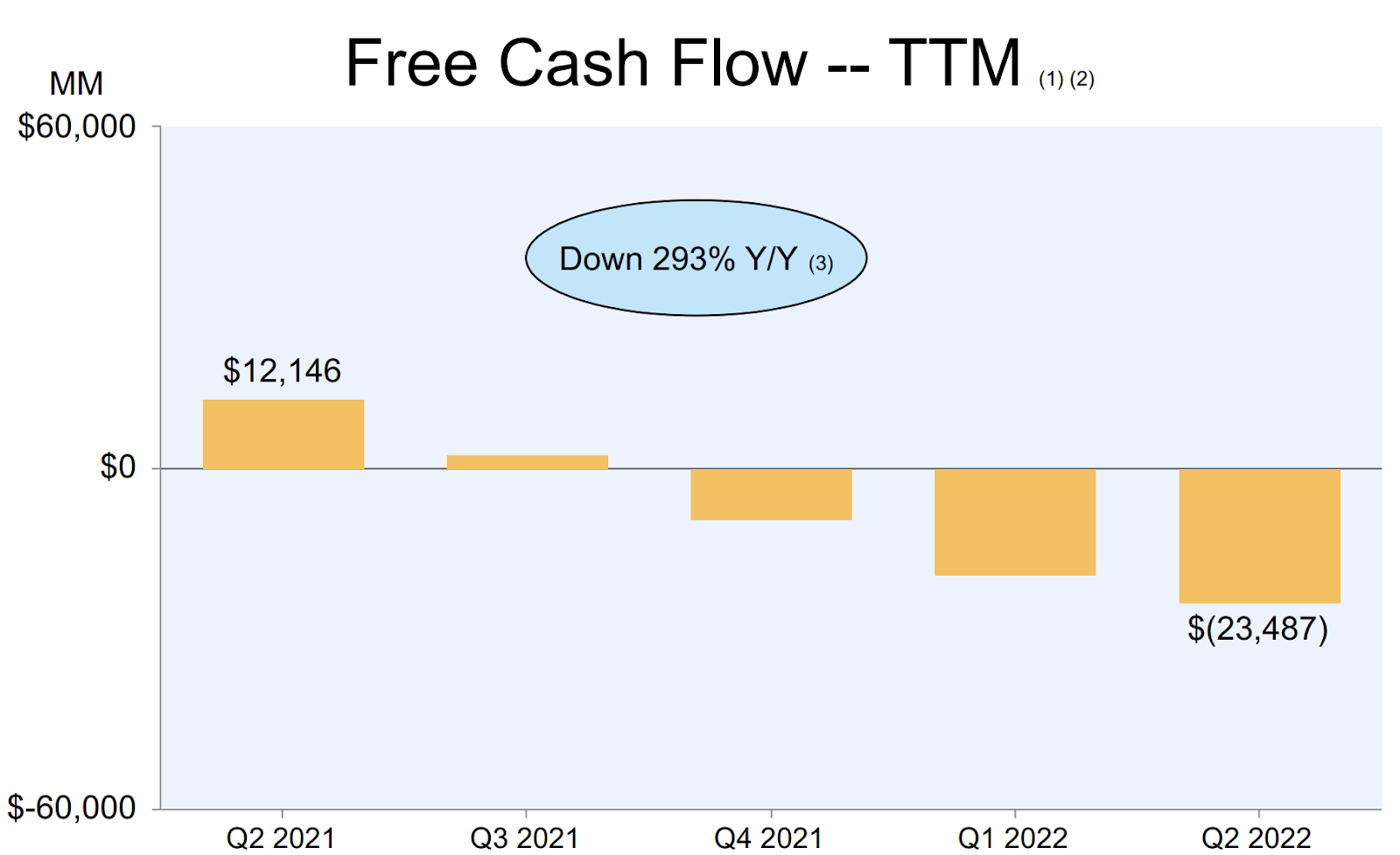

Source: Amazon’s Q2’22 Earnings

At its lowest point, Amazon was delivering negative 23 Billion in Free Cash Flow on a TTM basis. Yes, you’ve read that right, negative 23 Billion in FCF, back in Q2 of last year.

In the latest quarter, operating income is up 132% YoY, FCF has also finally swung back into the positive, and in my opinion, we will see explosive growth on the bottom line for Amazon in the coming few quarters as they continue to optimize their cost structure and exit from their heavy Capex spending era.

There is an ongoing drama between Amazon and the Federal Trade Commission (FTC) and Lina Khan, the head of FTC seems hell-bent on making a case to break Amazon up. It does seem like many of the lawsuits launched against Amazon are theatrics at best and the market is not buying it. For now.

On Amazon’s valuation, it’s a tricky business to evaluate. Many investors might be turned off by Amazon’s current price today at first glance; Forward PE of 63, P/FCF of 183x. Who in the right mind would want to own this stock?!

But at more than 1.4T in market capitalization, clearly, many investors still want a piece of it. I think we have to look at Amazon’s price on two fronts.

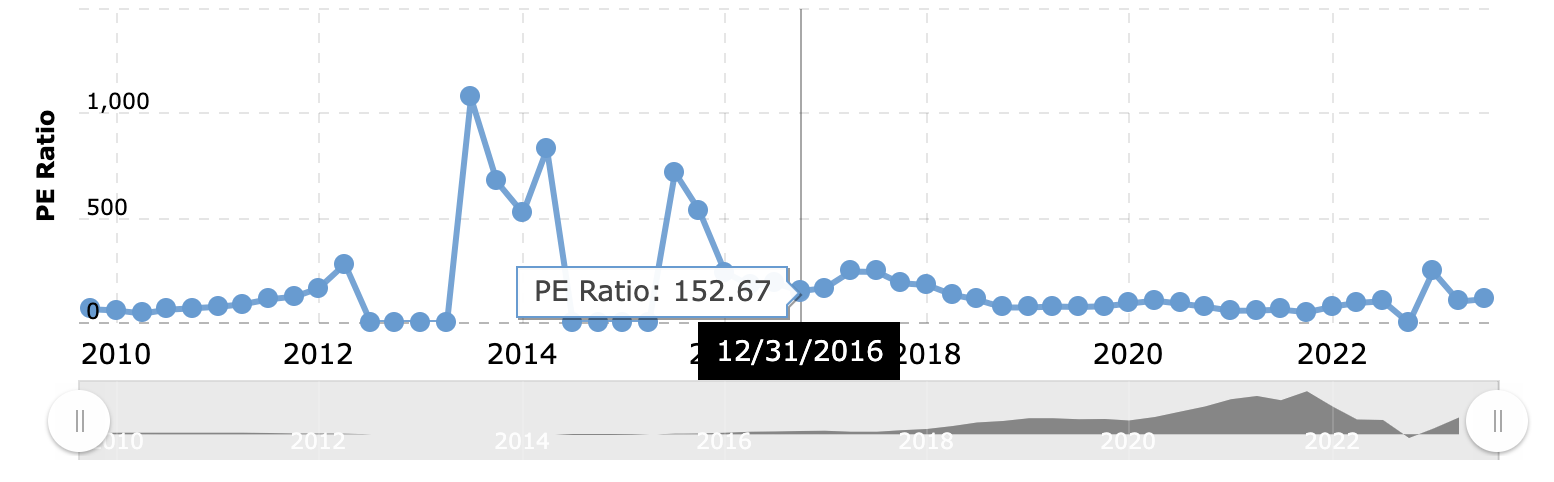

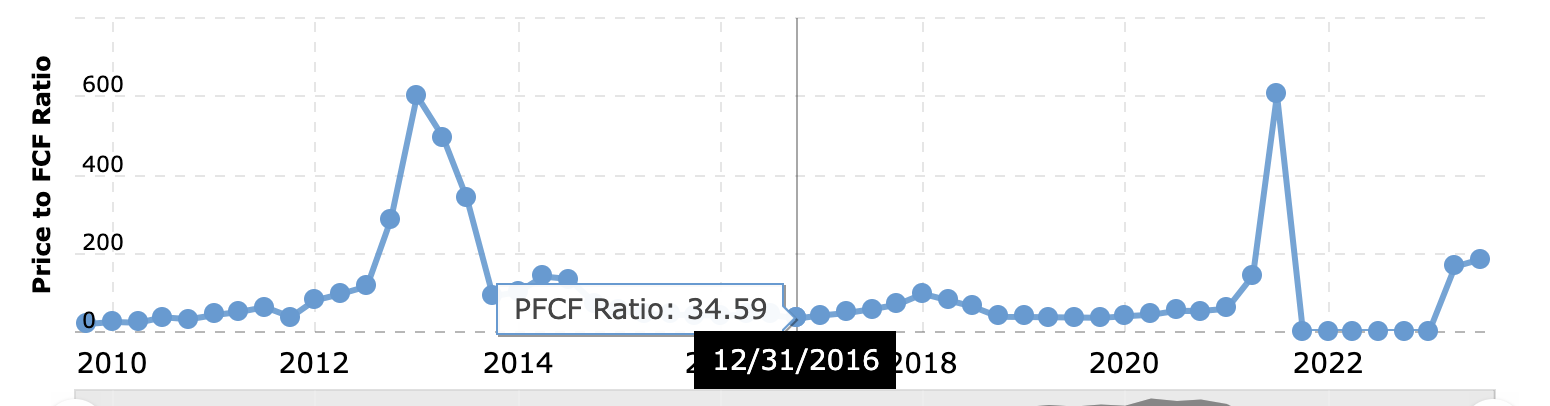

First, when we look at Amazon’s historical valuation patterns, they were never cheap to begin with. In the better part of 2014 through 2021, they were trading in a range of between 35 to 100x Price to FCF. At the lows, it was still less than a 3% FCF yield.

Source: Macrotrends, Amazon’s Historical PE Ratio

Source: Macrotrends, Amazon’s Historical P/FCF Ratio

Second, you can see that Amazon tends to experience such wild swings in their valuation also because their bottom line tends to be very noisy. To illustrate my point, the historical PE and P/FCF chart of Amazon tell the story. In a good year, they can be profitable, and in a bad one, they can swing to the negative as if they’re a start-up.

The bottom line is this, you will have to form an opinion on what the “real bottom line” profits Amazon is able to deliver as they continue to build out their cloud and commerce services.

Another realistic way is where some investors will use a sum-of-the-parts valuation model to evaluate this giant of an enterprise. In our opinion, we do find Amazon competitively priced with a slight margin of safety for investors who are interested. This is of course based on our assumptions that Amazon is going to recover strongly soon.

Is Microsoft (MSFT) a Good Stock to Buy Today?

Microsoft is probably one of the strongest businesses that we’ve seen in this decade. King of software, a portfolio across hardware, software, gaming, cloud, and even AI now. Some will see investing in Microsoft as being equivalent to buying into an exchange-traded fund due to its diversified nature.

A notable event that transpired that continues to plague Microsoft is the overhang on their intentions to buy Activision Blizzard, which is one of the world’s most valuable gaming companies for $68.7 billion. The original deadline for this merger was 18 July 2023, but we are well into mid-September and it still looks as if it is not slated to be completed anytime soon.

They were met with a series of challenges from legal to regulatory hurdles, and I hope the best for them in overcoming said obstacles. That said, buying over Activision or not will not make or break the investment thesis of Microsoft, therefore, I would not be too concerned about it.

Source: Yardeni Research

Source: Yardeni Research

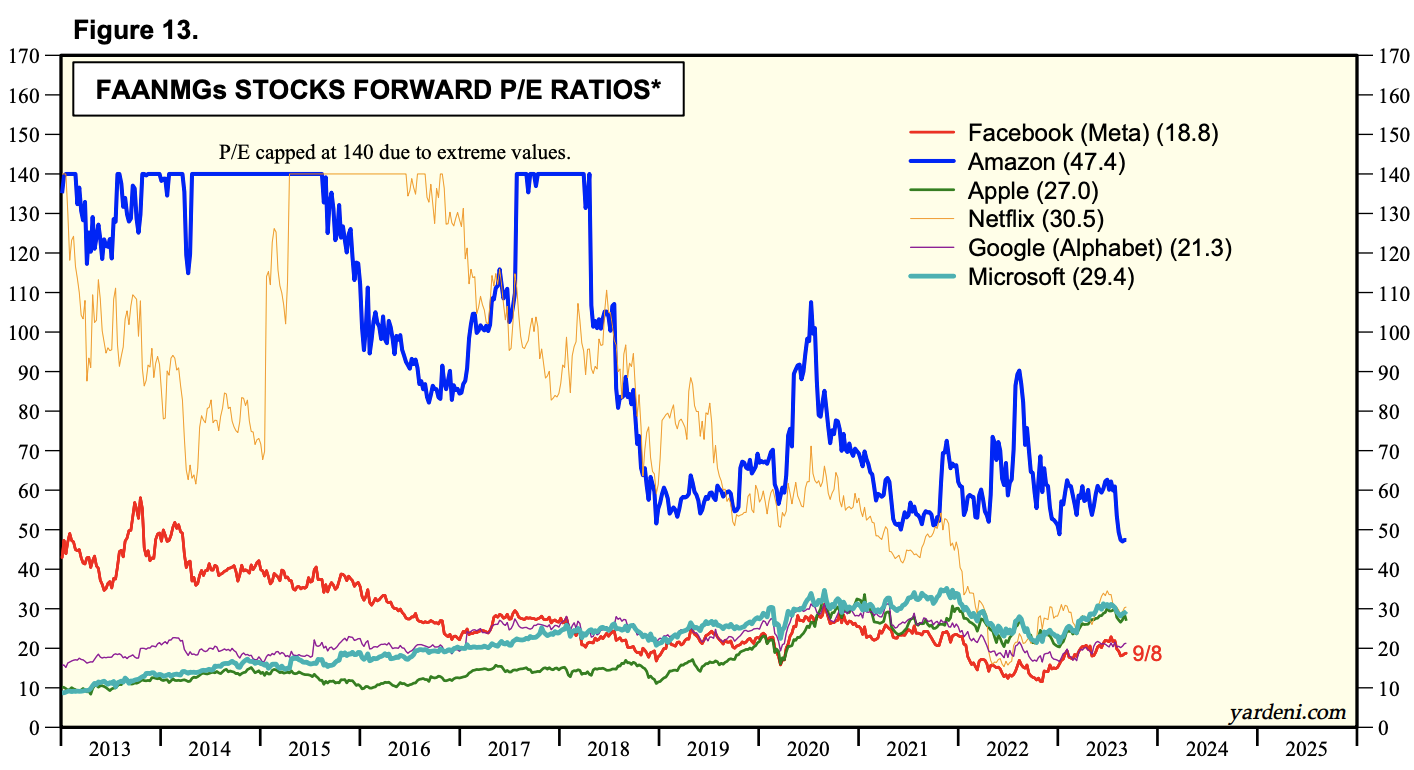

If I can hazard a guess, the only reason why many investors are having second thoughts about owning Microsoft today is because of their valuations. If we pit Microsoft against its FAANG counterparts, you can see that they are definitely trading in the premium range.

I think this is not to say that Microsoft is not worth a buy today, because it is clearly a wonderful business. For investors that have a really long-term mindset and can sit through the thick and thin with Microsoft, you can probably take a nibble at it, but not go all-in at current valuations.

As history has shown, there will always be unforeseen circumstances that hit your portfolio of companies, and if you made the assessment that many of these problems and challenges are short-term in nature, then those dips would be a good time to continue adding to the position.

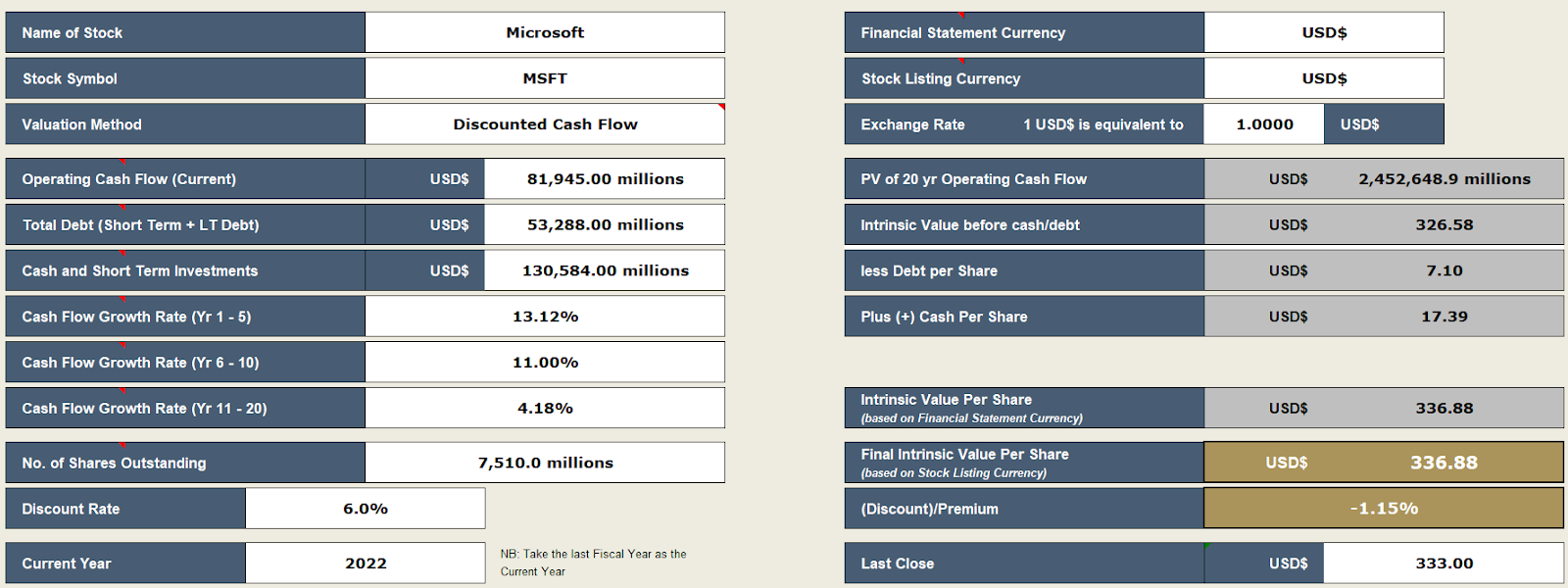

Source: Piranha Profits’ proprietary investing tool — the True Value Finder™

Based on our calculations, the intrinsic value of MSFT stock is right around $336.88 as of the date of this writing. Comparing it to the last close of $333, it is -1.15% below the IV, which suggests that Microsoft is hovering very close to its fair value.

As someone who loves a good bargain, I would like to buy Microsoft when it has a bigger margin of safety, but it will definitely be on my watchlist.

Is Alphabet (GOOGL) a Good Stock to Buy Today?

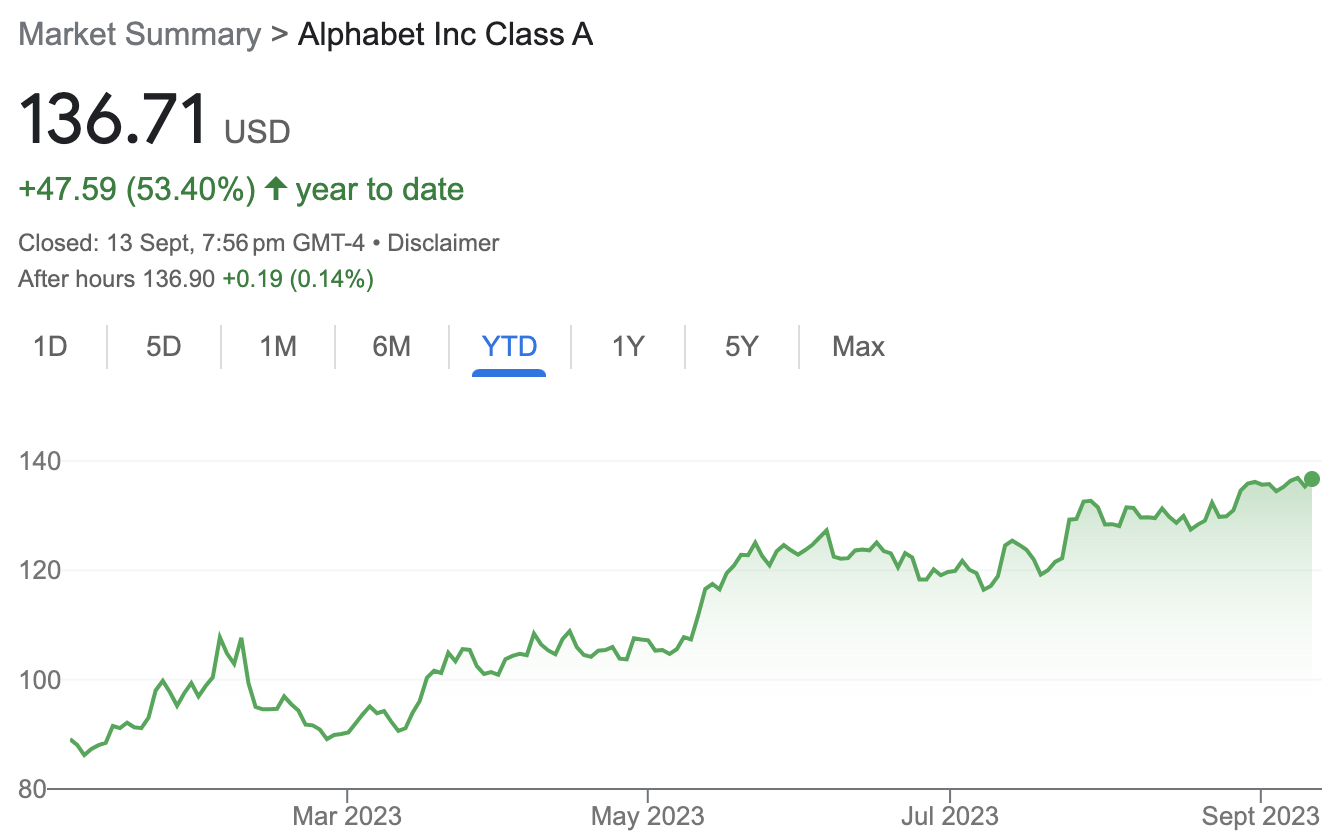

Source: Google Finance

The candidate with the weakest performance on a YTD basis is Alphabet (GOOGL), at right around 50% in the past 9 months. Yeap, 50% YTD appreciation and it’s the weakest performer, what a time to be alive in this market.

Anyhow, Google did not start the year out strong. Although it feels like eons ago, ChatGPT was only introduced in November last year and it took the world by storm, Google included. Upon a few iterations, Microsoft (who is a large investor of OpenAI which created ChatGPT) decided to integrate their large language model (LLM) into Bing, claiming it to be even more powerful than ChatGPT, and in Satya Nadella’s words “Make Google dance”.

Google’s response to that? Release their version of LLM — Bard. Long story short, the initial release was not as exciting as what investors hoped for, and to add on, there were notable errors caught during the presentation, causing investors to sell-down the stock because many were disappointed with the outcome of Alphabet’s high R&D spending only to push out a half-baked product.

To add, investors from all walks of life were confident that we are going to experience a recession some time soon. Google, being in the advertising industry, was primed for a major slowdown in growth as advertising is highly cyclical and models after the ebb and flow of the economy.

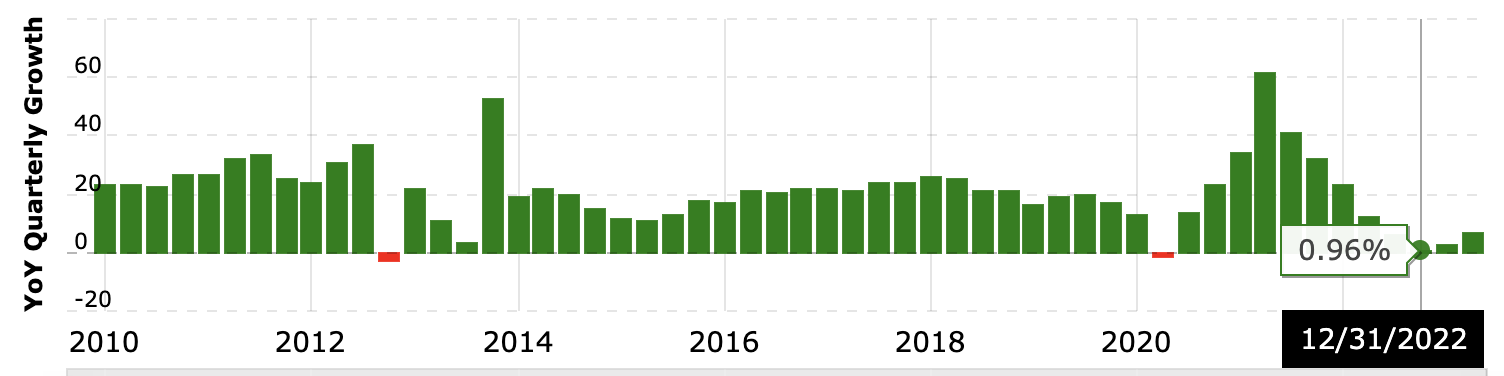

Source: Macrotrends

Google reported a revenue growth of 1% YoY for Q4 of 2022 earlier this year, triggering another round of sell-off as investors started turning pessimistic about the prospects of the business.

Weak growth, coupled with intense rivalry coming from a formidable competitor attempting to grab Google’s dominant position in Search was a double-whammy. In hindsight, we’ve come to appreciate that it might still be a little too early for users to completely adapt their workflow to one that is reliant on AI search results without verifying the veracity of the data themselves.

Also, it was reported that ChatGPT’s traffic had slipped again for the third month in a row, suggesting that Google might be in a much better position to retain their market share, contrary to what many investors initially thought.

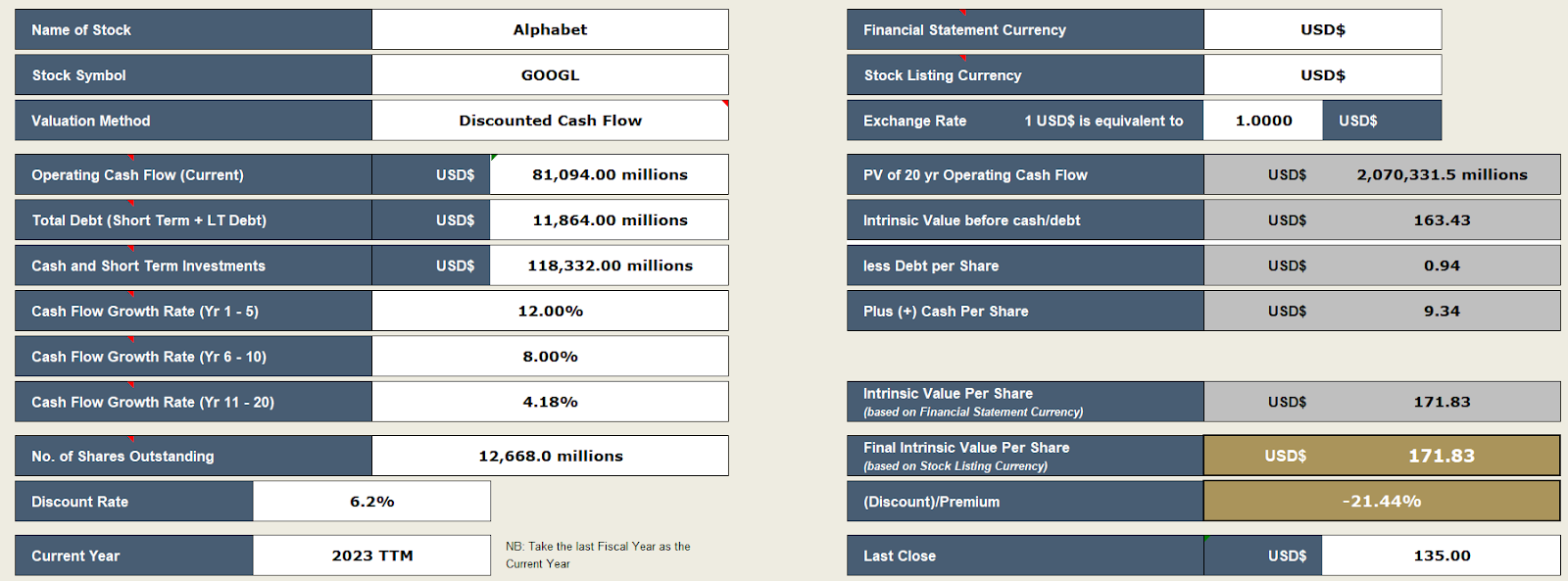

Source: Piranha Profits’ proprietary investing tool — the True Value Finder™

Based on our calculations, the intrinsic value of GOOGL stock is right around $171.83 as of the date of this writing. Comparing it to the last close of $135, it is -21.44% below the IV, which suggests that Alphabet is offering a relatively good level of discount over its IV today.

Google is currently trading at a 24x forward PE, with a FCF yield of around 4.1%. I don’t think it’s necessarily expensive, but it’s not dirt cheap either. We do still think that given the strength of Google’s fundamentals, it is still trading at a slight discount to its intrinsic value.

Is Meta Platforms (Meta) a Good Stock to Buy Today?

Source: Google Finance

Moving on to the next contender, another juggernaut in the advertising space — Meta, formerly known as Facebook. Meta has outdone Alphabet by a factor of nearly three times as they’ve experienced an appreciation of nearly 150%.

This spectacular performance came on the heels of a 75% decline back in 2022 from its peak due to a myriad of concerns from stagnating growth rates, to destruction in margins, to frivolous spending, to Mark Zuckerberg’s obsession with augmented reality and a sheer disregard for accruing shareholder’s value in any way thinkable.

At least, that was what most bears were arguing for in the better part of last year.

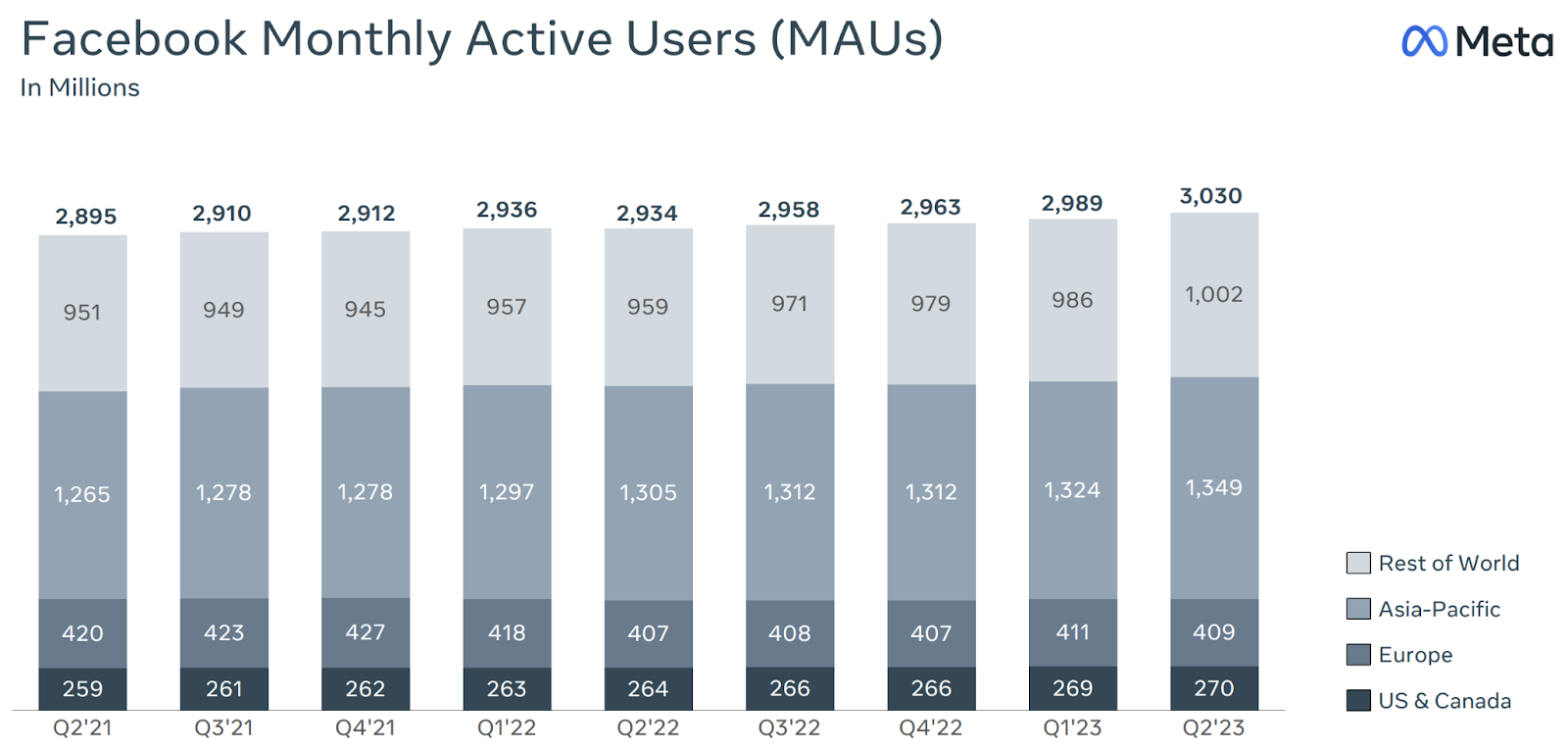

Source: Meta’s Q2’23 Earnings Report

In 2023 at least, the past few quarterly earnings have shown that there is a certain level of normalization in terms of both margins and bottom line. Further, they’ve squashed concerns in Meta being unable to acquire new users anymore as they’ve continued to show growth on both active users and ad impressions.

Zuckerberg has also clarified in multiple calls that a majority of their investments are into the AI capabilities of the legacy business, iterating and building on their existing Ads architecture, rather than simply blowing it all up in their AR/VR efforts. They’ve also come a long way in addressing concerns over the new Apple update which has heavily restricted their tracking and targeting of ads.

The icing on the cake was when Meta increased their share repurchase authorization by $40 billion, which worked out to around 10% of their market capitalization when it was announced, boosting confidence once again.

Despite Meta having a PE ratio of 36x now, the consensus estimate has their forward PE to be right around 22x with a FCF yield of only 3%. The TTM FCF yield might not be a very accurate representation as they experienced an identity crisis (so large that they had to change their company’s name) back in Q3 of last year, causing their FCF to essentially evaporate. Anyhow, Meta was also in that period of spending large amounts of capital expenditure, causing a large hit to their bottom line.

We are optimistic of Meta swinging back to being highly profitable and cash-generative again but investors must be comfortable with Zuckerberg’s money-losing pet project on the side as they’ve committed that there will be increasing cash burn set aside for the reality labs segment.

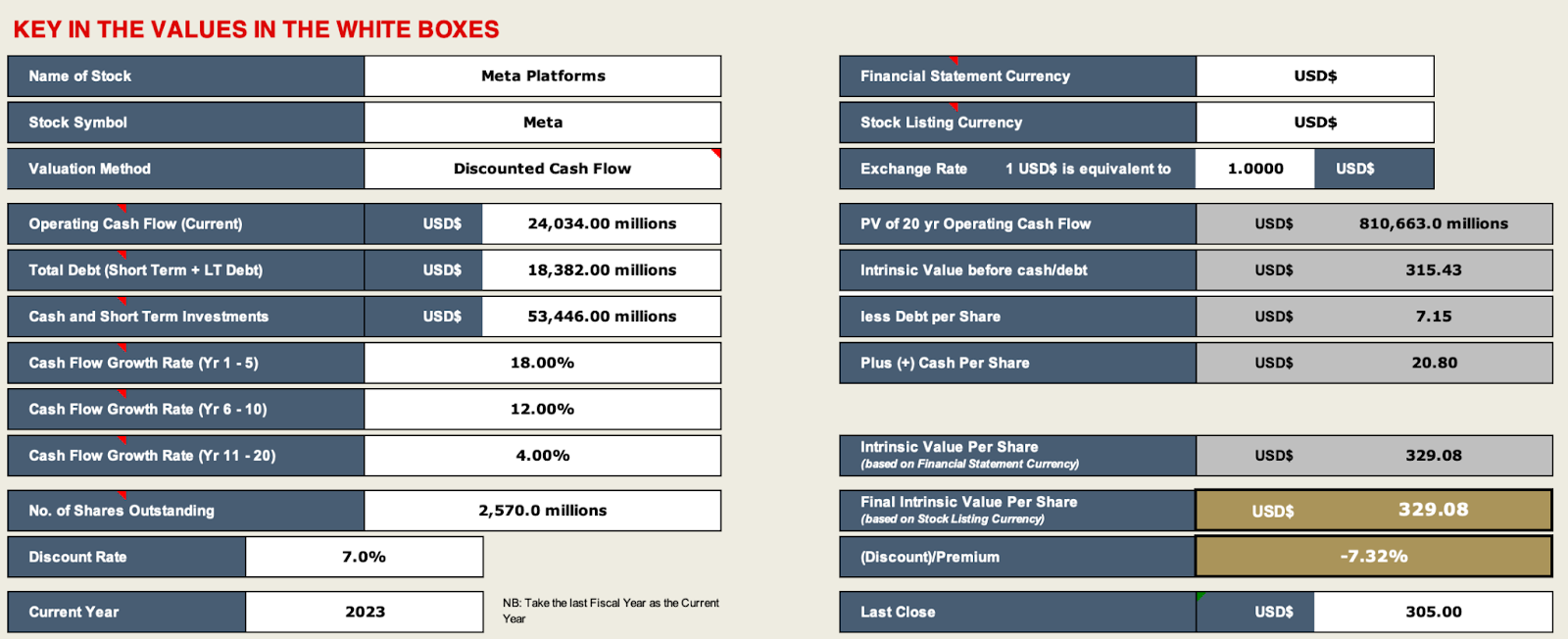

Source: Piranha Profits’ proprietary investing tool — the True Value Finder™

Based on our calculations, the intrinsic value of Meta stock is right around $329 as of the date of this writing. Comparing it to the last close of $305, it is -7.32% below the IV, which suggests that Meta is probably right around fair value territory.

For Meta’s valuation, even after this phenomenal run-up, I don’t suppose that they’re trading at an egregious valuation. If I can speculate, the reason why both Alphabet and Meta trades at relatively lower valuations compared to the Big Tech is because other Big Tech (namely Apple, Microsoft and Amazon) are now zero-ing into the advertising industry.

Given conservative estimates, Meta’s intrinsic value for us sits at around $280 to $330, and we would want to wait for further pullbacks before adding to them anytime soon.

Is NVIDIA (NVDA) a Good Stock to Buy Today?

Source: Google Finance

NVIDIA — arguably the only company that has truly benefited from this entire AI craze that flowed through to their earnings and cash flows. Last quarter, they grew revenue by 101% and net income by 843%. These are not rookie numbers, especially for a company that is already established with a high base.

When talking about NVIDIA, you will probably meet two different groups of investors. One group completely writes them off as they cannot make sense of their current valuations using a rear-view mirror when looking at their historical earnings. They’re trading at a PE of 108x, P/S of 34x and P/CF of 93x. Their forward price ratios look better as the street estimates NVIDIA to continue delivering this sort of crazy growth.

Meanwhile, the other group is extremely optimistic about the future of AI, GPUs and the software-hardware integration of NVIDIA — crowning it the iPhone moment of NVIDIA.

Truth be told, I’m somewhere in between. I don’t think we should throw the baby out with the bathwater. Yes, I acknowledge that there are many companies that are jumping on the AI bandwagon recently and the markets have traded their stock wildly. For NVIDIA’s case, I’ve watched and listened to many intelligent investors make their case for investing into it. Reasons ranging from the superior software-hardware integration, to phenomenal foresight in their forays before their competitors in both crypto and AI.

Although I am a big believer in AI being the next frontier of innovation, I’m not so sure if investors are getting too ahead of themselves. Sure, NVIDIA has blown expectations out of the water over the last two quarters and would likely continue to do so in the following two quarters based on management’s guidance. However, there is really not much visibility on how sustainable this growth will be.

Some argue that growth in the short term is artificially boosted by these major Chinese players shoring up NVIDIA’s chips before the ban, while others think that AI is the way to go and it will turn into a blanket tax for all tech companies moving forward. Who knows?

Source: Macrotrends

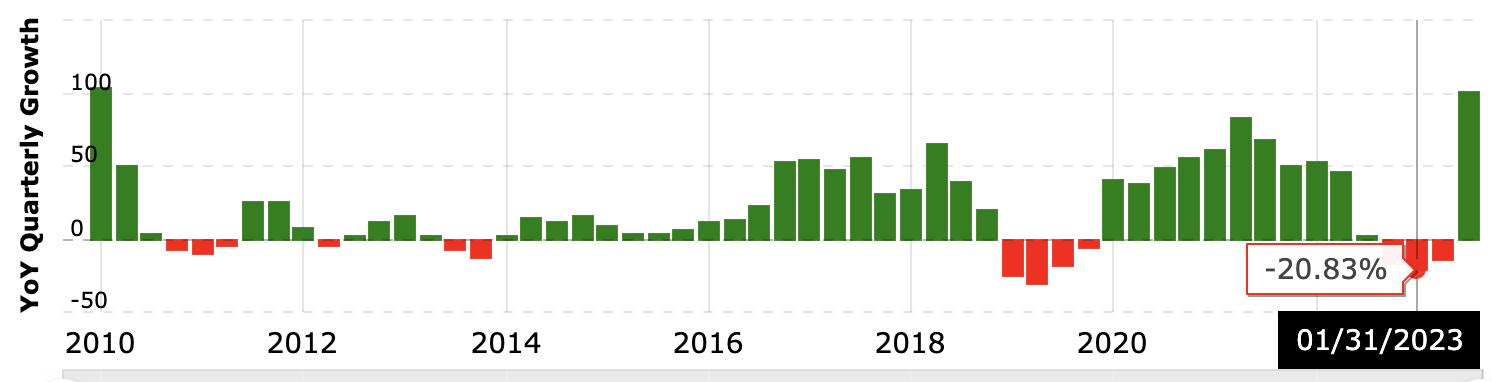

Let’s not forget that just a few quarters back, NVIDIA saw a revenue growth of -20% YoY for their January 2023 earnings as their sales took a hit mostly attributable to the crypto winter. Yes, AI and data centers are the big talk in town now, but how long can it last? That is why investing is so interesting yet challenging most of the time.

There are many analysts who have price targets and valuation models around NVIDIA today, but I think most of them will probably miss the mark. Therefore, whether NVIDIA is a buy today really depends on how aggressive or conservative your assumptions and estimates are. Personally, I do find NVIDIA’s current valuation on the high side. And I mean the sky-high side.

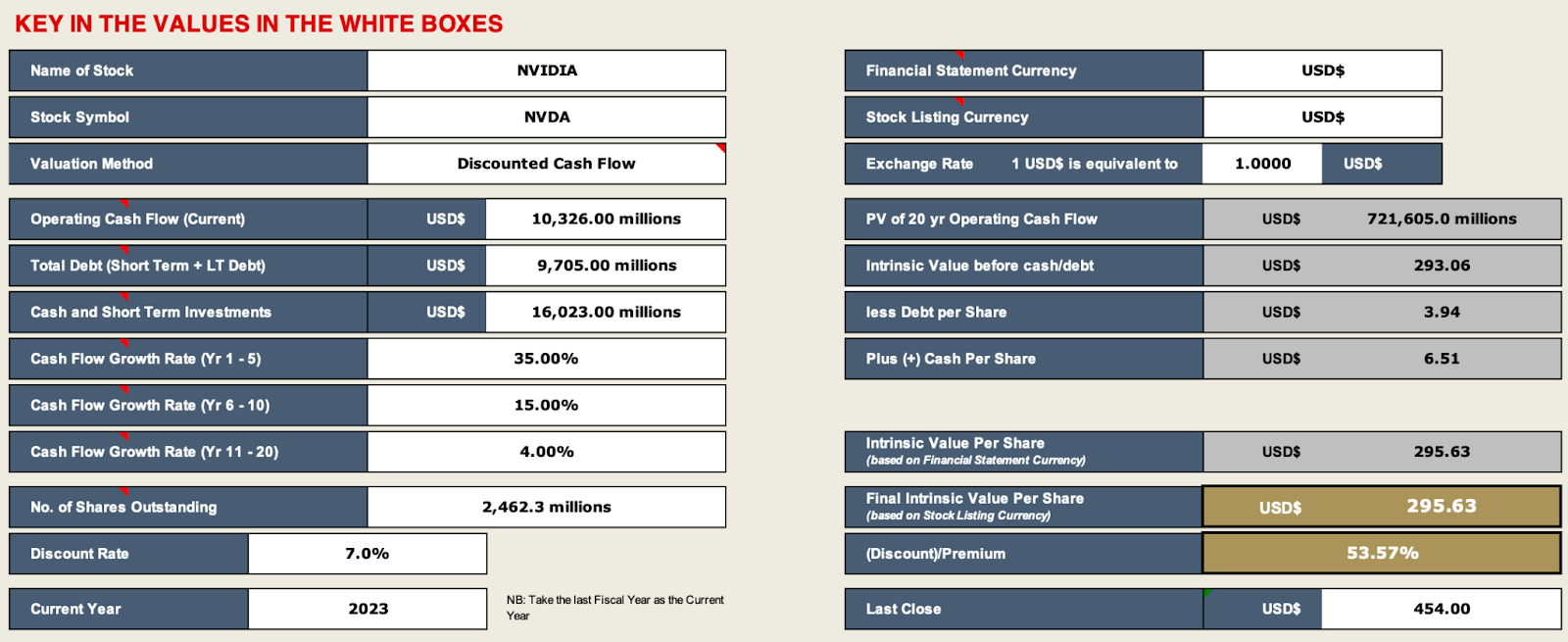

Source: Piranha Profits’ proprietary investing tool — the True Value Finder™

Based on our calculations, the intrinsic value of NVIDIA stock is right around $300 as of the date of this writing. Comparing this to the last close of $454 per share, it is more than 50% overvalued.

For traders, I think NVIDIA has got good momentum. For investors who want to buy and hold, I think we can wait for a few more quarters to see how NVIDIA continues to perform as the excitement dies down with time.

Is Tesla (TSLA) a Good Stock to Buy Today?

Source: Google Finance

Like it or not, I will end up offending one group of investors or another by having an opinion on this company, so I will tread carefully on this popular stock.

Tesla has had phenomenal success and execution over the last few years. The stock price aside, I think the company has executed superbly. To understand Tesla’s valuation today, it really depends on how you see the future of the company.

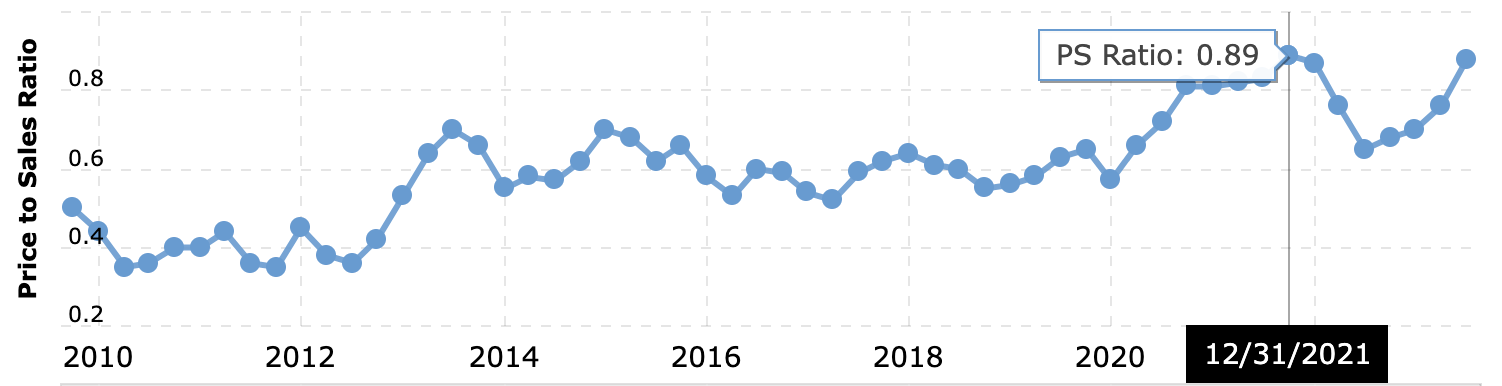

On the bearish side, if you view Tesla as solely a car company, today’s valuations might look a little lofty as they sit at a Price to Sales of around 10x, while comparable companies like Toyota, Ford and GM have PS ratios of only 0.3 to 1x.

Source: Macrotrends, Toyota’s Price to Sales

Some might argue that even if you look at Tesla as only a car company, you should compare it to Ferrari because they too have a relatively high valuation. Personally, I disagree; the nature of how they conduct their businesses are fundamentally different. Tesla is no longer even trying to compete with the premium segment of the car anymore — they just want to sell to everyone, everywhere.

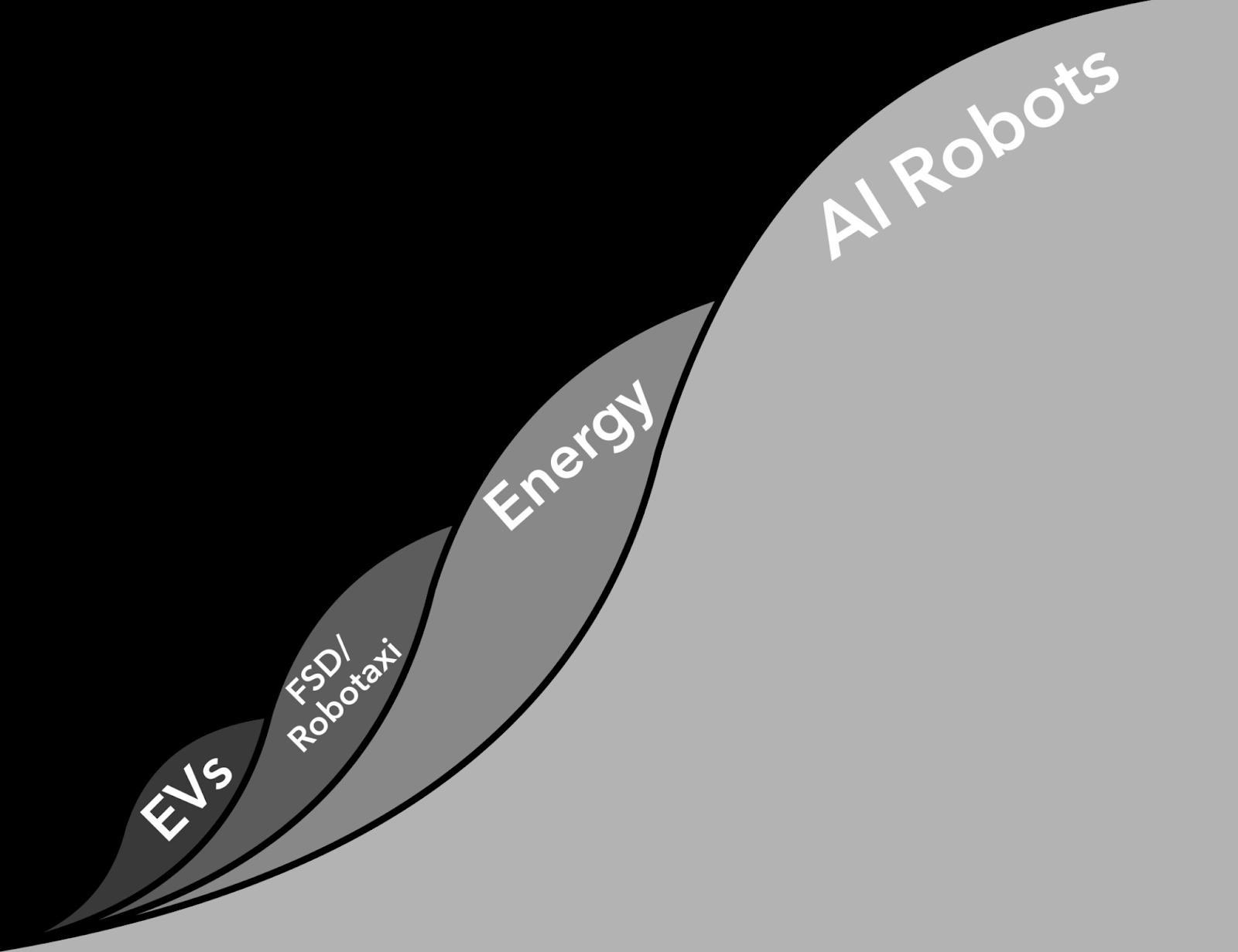

However, if you were to ask the bulls, they will be showing you the other side of the story where the car is just a trojan horse for Tesla to sell you something better. Like FSD, to Energy, to even robotics in the future. Tesla is right at the start of multiple S-curves as they claim.

Just last week, an analyst report coming from Morgan Stanley upgraded Tesla to an overweight, coupled with a price target of $400 per share due to their AI Mojo project. This was very well received by the market because who doesn’t want confirmation from Wall Street, right?

Anyway, we do believe that Tesla is working on exciting projects and Elon Musk is someone that I probably don’t want to bet against. But let’s still be clear that many of the claims are still claims. I would highly encourage you to watch a livestream by Musk himself on X about the current state of Tesla’s FSD capabilities.

The bottom line, if you believe that Tesla is only a car company, then today’s valuation might be on the lofty side as the old argument of Tesla having the highest margins in the auto industry is slowly falling apart.

However, if you do think that Tesla is able to continue building out its energy and FSD business, then today’s earnings will pale in comparison to their future potential (assuming that no one else can come close to providing an alternative).

All in all, we believe that there are still undervalued gems hidden in the Magnificent Seven names, especially if you are able to do your own valuation work, and study the companies in-depth.

If you’d like a powerful tool that tells you the right price to enter these stocks, do check out our True Value Finder™ and learn to find undervalued deals with confidence.

Till next time, Keep Winning.

submit your comment