Sea Limited (SE) stock used to be a darling of Wall Street — a source of pride for many growth investors as the stock had increased more than 20-fold in a short span of 4 years from IPO to peak.

Initially, the growth story of Sea Limited was predicated on the “3-headed dragon” analogy, with three strong engines of growth that had a huge runway, namely: ECommerce, Gaming and Digital Finance.

That said, Sea Limited has since corrected by nearly 90% from its peak and many investors are wondering if Sea Limited stock is a buy now.

Table of Contents:

Why is Sea Limited (SE) Stock Dropping so Badly?

Why is Sea Limited (SE) Stock Dropping so Badly?

Sea’s Gaming Business (Garena) was DECIMATED

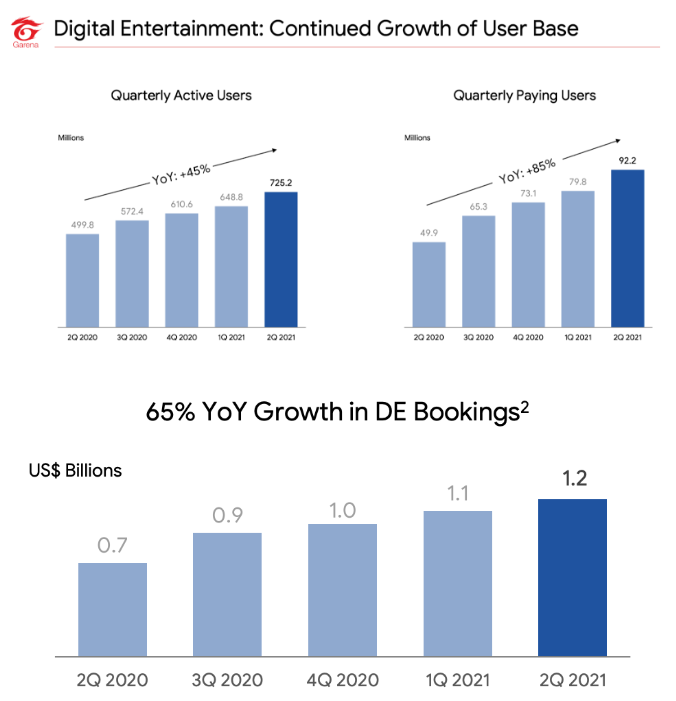

Source: Sea Limited’s Q2’21 Earnings Presentation

Many believe that a picture speaks a thousand words. Let’s run this experiment. Based on the two infographics that were extracted from Sea’s earnings presentation back in 2021, what does it tell you about their gaming business?

They look good, right? Heck, it was phenomenal. Many companies would kill to have such growth and profitability.

Let’s take a look two years later…

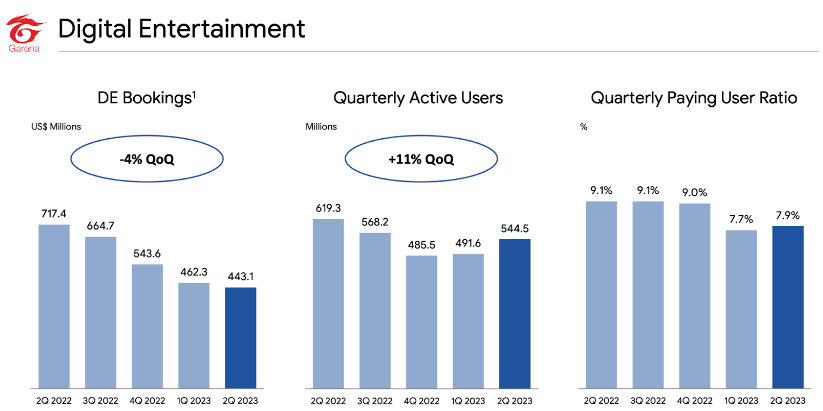

Source: Sea Limited’s Q2’23 Earnings Presentation

This was Sea gaming division's latest result. I do have three words to describe this development:

Under the sea… (pun intended😜)

Jokes aside, you can see that Garena has suffered greatly from losses in bookings, quarterly active users and by translation, quarterly paying users. Their bookings fell by 66% due to two main reasons.

Firstly, Garena has always been extremely reliant on their core offer League of Legends (LoL), but Riot Games (owner of LoL) has recently decided to self-publish the title in Southeast Asia from January 2023 onwards.

Secondly, another hit piece Free Fire was banned in India, which so happens to be one of their biggest and most profitable geography. The reasons for the ban is unknown, but the word on the street is that India is taking decisive actions against China, and despite Sea Limited being a Singapore company, the founder was born in China who subsequently moved to Singapore.

On a brighter note, the ban was instituted back in February 2022, and we’ve seen Garena numbers deteriorate for more than a year now, and it does seem like quarterly active users have bottomed out in Q4 of 2022. It would probably be prudent to do any subsequent projections and modeling on this new base figure.

Sea Limited Was a Cash Incinerator All Its Life

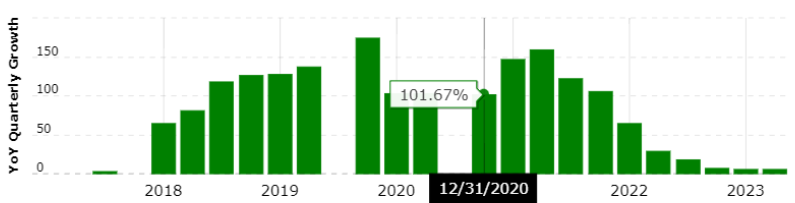

Source: Macrotrends, SEA Limited Growth rates

Pre-2022, Sea Limited was known in the investment world as the company that only delivered triple-digit growth rates. Anything less was something worth frowning upon, and they had managed to keep up with this track record from 2018 to 2021, excluding Covid impacts.

In order for Sea Limited to deliver such growth, they did it at the expense of profitability. In fact, I would argue that they were incinerating cash as if money dropped from the sky.

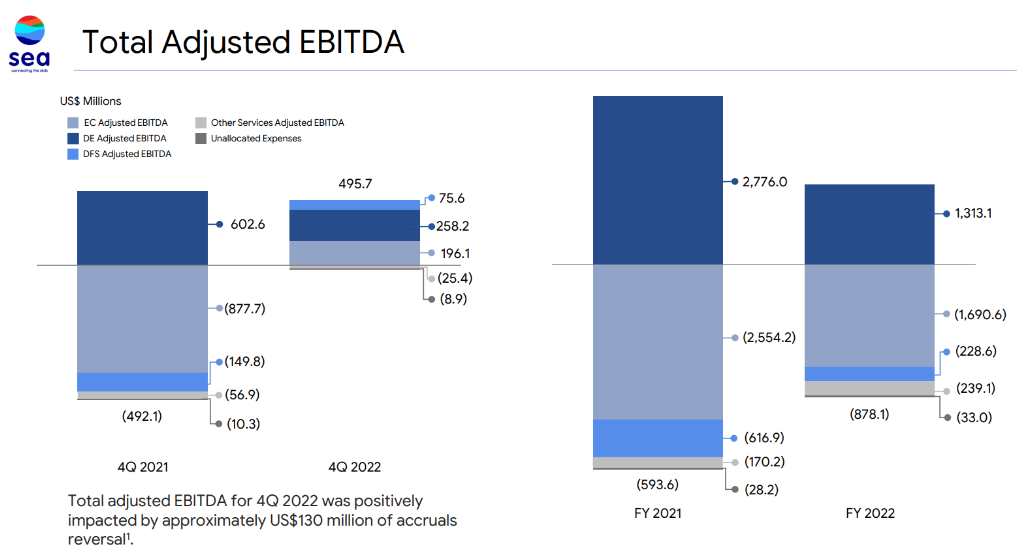

Source: Sea Limited’s Q4’22 Earnings Presentation

Just a snapshot from their FY 2021 and 2022 numbers would show you that they are perfectly comfortable with delivering a negative bottom line, as long as they had the top line to show for.

However, alarm bells started ringing when their gaming business (which was the only profitable segment) was experiencing life-threatening challenges. Without the “subsidy” from Garena, Sea Limited’s bottom line was plain out disgusting — losing more than 2 billion USD per year in 2021 and 2022.

This was coupled with the fact that the US Federal Reserve has been raising rates at an unprecedented pace — many high growth, unprofitable companies were at the mercy of Jerome Powell as the environment to raise capital and grow became exponentially harder.

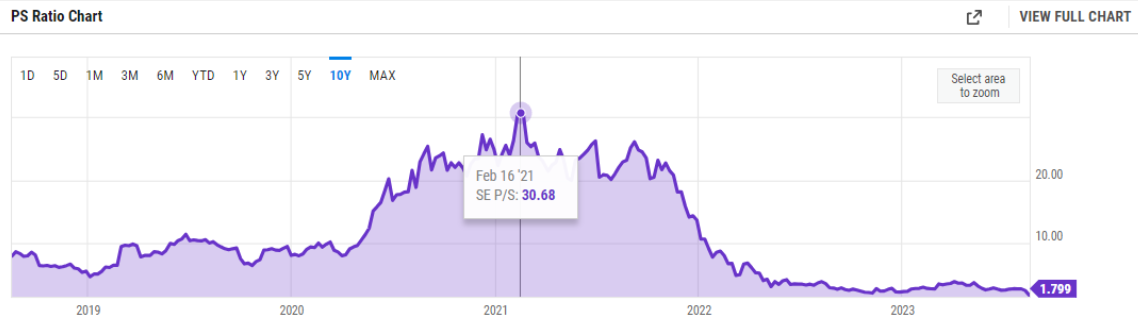

The Market Was Too Optimistic of Sea Limited’s Growth Trajectory

Source: Ycharts, SEA Limited’s PS Ratio

At its peak, Sea Limited was trading at more than 30x Price to Sales.

We’re talking about sales by the way; there were no profits to begin with. Many are probably expecting Sea Limited to be able to deliver on the stellar growth rates they’ve done in the past, hence investors were willing to pay a premium for it, but there is still a price too high to pay.

Given the macroeconomic context Sea Limited was in, they had to pursue a different strategy moving forward. Since cheap capital was no longer readily available, they do have a limited time to quickly cut back on expenses and focus on profitability instead as they are hanging on a thin thread with their balance sheet capacity.

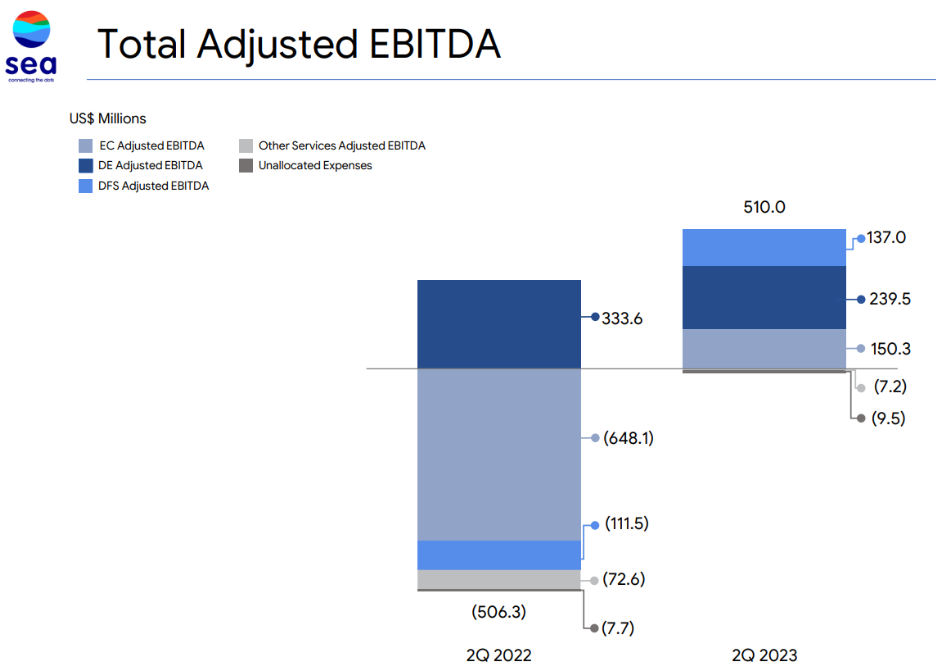

Source: SEA Limited’s Q2’23 Earnings Presentation

In the latest quarter, the management team over at Sea has WoW-ed investors again with their focus and execution. Within a few short months, all three business segments have turned EBITDA profitable.

However, investors did not seem to like it at all because it came at the expense of the overall growth of the company. They’ve managed to only grow 5% top line revenue (with Ecommerce +20.6%, Gaming -41%, Finance +53%).

On a brighter note, Sea’s cash balance has started trending upwards again, suggesting that they will not be in a precarious position to urgently raise money to sustain their operations.

We’ve seen some commentaries stating that Sea Limited used to be burning through cash, and now that they’ve proven themselves to investors that they can turn profitable, the markets still chose to punish them (by selling down the stock).

We think that it is more meaningful to look at the entire picture.

Sea Limited’s story was really predicated on being the dominating force of both Ecommerce and Gaming in the Southeast Asia region, especially with the HUGE total addressable market (TAM) and long runway ahead. Although they’ve turned EBITDA profitable, it was at the expense of growth, and the story of Sea being able to capture a large part of this TAM is under scrutiny now.

Layer that on with the difference in investor psychology — early SE stock investors were most probably growth investors. Would they still put their capital in a company that is only growing their top line at 5% YoY when there are many more other candidates out there? We doubt so.

Therefore, it does seem like there is a change in the shareholder structure from one of growth to one of value, and the “value” of Sea Limited today is contingent on how you evaluate the team on managing this inflexion point.

My Worries with Sea Limited (SE) Stock Today

Now that we understand what transpired with Sea Limited’s story, I think it’s an opportune time for us to express our concerns around the environment they are in today.

Sea Limited (SE) Stock Forecast: It’s Not at All Rosy

An analyst from Citi recently lowered her rating on Sea Limited from a buy to a neutral — slashing her price target from $98 to $50 — while noting that the company is undergoing a strategy shift and that there will be a “brutal battle” to defend its market share.

In the recent earnings call, Sea’s management expects ongoing “reaccelerated” investment to defend and grow their market position. Shopee’s biggest competitor in Southeast Asia, Lazada, has recently received $845 million in funding from parent company Alibaba.

This constant investment and pressure do signal to investors that there will be even more challenging and bumpy roads ahead for the industry. Furthermore, Lazada does have a much stronger financial backing from Alibaba Group, while Shopee on the other hand is struggling to get more support from Garena as outlined by the circumstances above.

For a fun fact, with Alibaba Group’s current CASH position, they are able to buy out the entire Sea Limited company THREE times. That’s the contrast in financial power we are talking about.

That said, in the game of business, the company with more money might not necessarily win, and we’ve seen this play out time and again. At least in the last five years, Shopee had managed to pull its weight against its competition by coming up on top, even surpassing Lazada which had the first-mover advantage.

The bigger question would be if they are able to maintain their lead even with lesser funding moving forward.

SeaMoney Is a Black Box Mystery

With the Ecommerce business slowing down ever so slightly, investors are currently amplifying the role of SeaMoney, which purports to be the next growth engine for Sea Limited.

In fact, there are some investors with the thesis that Sea Limited is able to replicate the close-loop ecosystem that some of its Chinese counterparts have created, like Alibaba or Tencent, making them the “everything app”.

We would caution against such comparison as it does seem like every tech company today wishes to be the “super-app”, like PayPal, Grab, X (formerly known as Twitter) and more… Further, circumstances are largely different in where SeaMoney is operating in (11 countries) versus Tencent/Alibaba which operates mostly in China, and so are the objectives of the different governments.

We are therefore skeptical of SeaMoney achieving what Tencent Pay or Alipay has achieved in China.

Although it is true that Sea, like Alibaba, dabbles in very similar industries and they are able to learn a thing or two from Alibaba’s playbook, execution and timing is probably everything.

There is a relatively good story for the FinTech arm as they penetrate into the less-developed economies where there are good opportunities to serve the unbanked and underdeveloped. However, in the recent report, we are seeing a mismatch between numbers and story as there is a substantial deceleration in growth.

|

Quarter / FY |

YoY Growth Rates |

|

Q2 FY2022 |

214% |

|

Q3 FY2022 |

147% |

|

Q4 FY2022 |

92% |

|

Q1 FY2023 |

75% |

|

Q2 FY2023 |

53% |

It does seem like the thesis of a ginormous TAM in the Digital Finance space waiting to be conquered is slowly breaking down as SeaMoney is unable to capture that growth. As the stock price came plummeting down, investors started reflecting on the story that they were sold on, comparing whether the numbers measured up.

Also, investors will have to get comfortable with their forays into the lending industry where loans and credit risk will be assumed by the company on a very large scale as the company continues to grow.

Sea Limited (SE) Stock Forecast: Is It a Good Time to Buy Now?

Here’s the bottom line.

Sea Limited is in a fairly interesting position. Their recent strategy maneuver was essential due to the macro conditions, pivoting from growth to profitability, but it left a sour taste in many investors because that was not what they’ve signed up for.

Sea’s management has proven to shareholders that they are able to deliver bottom line profits when staying afloat is called into question. However, the current atmosphere amongst investors is that many believe now is not the right time to focus on profitability. There is still much more room for Sea to grow into, while at the same time, opportunities to expand the moat around the company.

The recent shakeout was a rude awakening to many investors on why growth investing is particularly difficult as expectations will oftentimes mismatch with reality.

For now, the current consensus is that Sea is going to have a particularly hard time competing, especially when the economic moat of Sea Limited is not well-established. Backing Sea today is basically betting that they are able to re-accelerate the growth in both the Ecommerce and Digital Finance business.

I would argue that even though we are seeing signs of bottoming and consolidation for the Gaming business, I am not placing much emphasis and expectations on them to accrue any meaningful shareholder value. Garena’s job now is just to soften the blow of Sea’s expansion strategy.

Given that the management at Sea has signaled to investors that they will be accelerating investments to growth, we can probably expect their bottom line to take a hit again sometime soon. For 2023 at least, I believe that they are going to keep to their word on delivering profitability (at least to show investors that they can).

This is assuming that they are able to continue maintaining this level of profitability — $500 million in adjusted EBITDA per quarter. That means that Sea Limited is trading at around 11 to 14x EBITDA. It is definitely not an “expensive valuation” to pay (for a growth company), but it is purely contingent on whether Sea Limited is able to deliver growth again.

We would reckon that as Sea Limited is not a company with a wide economic moat yet, investors would probably classify Sea as a speculative bet on a portfolio level. Given how the management team has described their game plan, you have to be ready when Sea Limited swings back to being highly unprofitable again. The determining factor would then rest on whether Sea is able to build their moat with high-quality growth that is accrual to the business in the long-run.

If you are interested to find out companies that we deem to have wide economic moats that are currently in our portfolio or watchlist, do check out the Ultimate Investors Playbook where Adam Khoo has done deep-dive analysis on strong potential companies that will make it into your watchlist.

Till the next time, Keep Winning.

submit your comment