Imagine an insurance policy. Someone pays a premium today. As long as nothing bad happens before the policy expires, the seller keeps every cent (premium). That is roughly how a credit spread behaves for an options trader, except instead of writing a single, unlimited-risk policy, the trader also buys a cheaper "reinsurance" contract that caps the worst-case scenario.

This guide walks through the credit spread definition, the mechanics, an example, the psychology that often comes up with the strategy, and the risks that traders generally plan for.

What Is a Credit Spread?

A credit spread is an options strategy where a trader sells one option and simultaneously buys a cheaper option of the same type (both calls or both puts), typically with the same expiration but a different strike price. Because the option being sold collects more premium than the option being bought costs, a net credit is received on day one.

And that credit the trader receives is the maximum profit on the trade. Just like the insurance company in the above analogy provided.

If you are familiar with Options trading basics, the meaning of credit spread is basically: a defined-risk, two-leg trade designed to pay the trader to be approximately right about a direction, rather than paying out money to bet on it.

Credit spreads usually point to one of two structures. A bull put spread is built from puts and tends to profit when the stock stays above a certain level. A bear call spread is built from calls and tends to profit when the stock stays below a certain level. Both share the same DNA: short the closer-to-money option, long the farther-from-money option, collect a net credit, define the risk.

How a Credit Spread Works (The Mechanics)

A credit spread has four variables.

The Two Legs

A credit spread is built from two options of the same class:

1. The short leg. This is the option being sold. It carries the higher premium because it is closer to the current stock price (and therefore more likely to be exercised against the trader).

2. The long leg. This is the option being bought. It is further out of the money, so it costs less. Its function is not to make money, but to cap the maximum loss if the trade goes wrong.

Selling the short leg generates a premium. Buying the long leg costs a smaller premium. The difference is the credit kept when the position is opened. That credit lands in the account immediately.

If you are new to Options Trading, refer to our Beginner Options Trading Guide.

The Width of the Spread

The distance between the two strike prices is called the width of the spread. A $100 short put and a $95 long put has a width of $5. Because each standard option controls 100 shares, the dollar width is $500.

This number drives the maximum risk on the trade. The math is fixed:

Maximum profit = the net credit collected (in dollar terms, the credit per share times 100)

Maximum loss = (width of the spread) minus (the net credit), again multiplied by 100

So a $1.20 credit on a $5-wide spread is risking $3.80 to make $1.20 per share. That is $380 of risk for $120 of reward. The reward-to-risk ratio may look skewed, but probability tends to be on the trader's side: the stock only needs to stay on the favourable side of the short strike for the spread to win.

The Expiration of a Credit Spread (DTE)

Credit spreads are time-decay trades. This basically means that every day that passes, the value of both options will drop (if all else stays equal).

Because the short option is closer to the money, it typically loses value faster than the long option. That asymmetric decay is what generates profit over time. As a credit spread trader, you only realised your full profit by holding it all the way and the price stays within range.

However, this does not mean that you can’t exit the trade if the contract already realised majority of the credit earned. Options trader can buy to close the position and keep the credit earned so far if the underlying stock thesis changes and there is a higher possibility of sudden movement.

The Outcome at Expiration of a Credit Spread

There are three ways a credit spread can end:

1. Both options expire worthless. The trader keeps the full credit. Effectively the best case scenario.

2. The short option finishes in the money and the long option finishes out of the money. The result is a partial loss somewhere between zero and the maximum loss.

3. Both options finish in the money. The result is the full maximum loss.

The downside is bounded. There is no infinite downside, no naked-options margin call. The risk is defined the moment the trade opens, and that’s the feature of a credit spread. To further explain, let's explore an example of a credit spread.

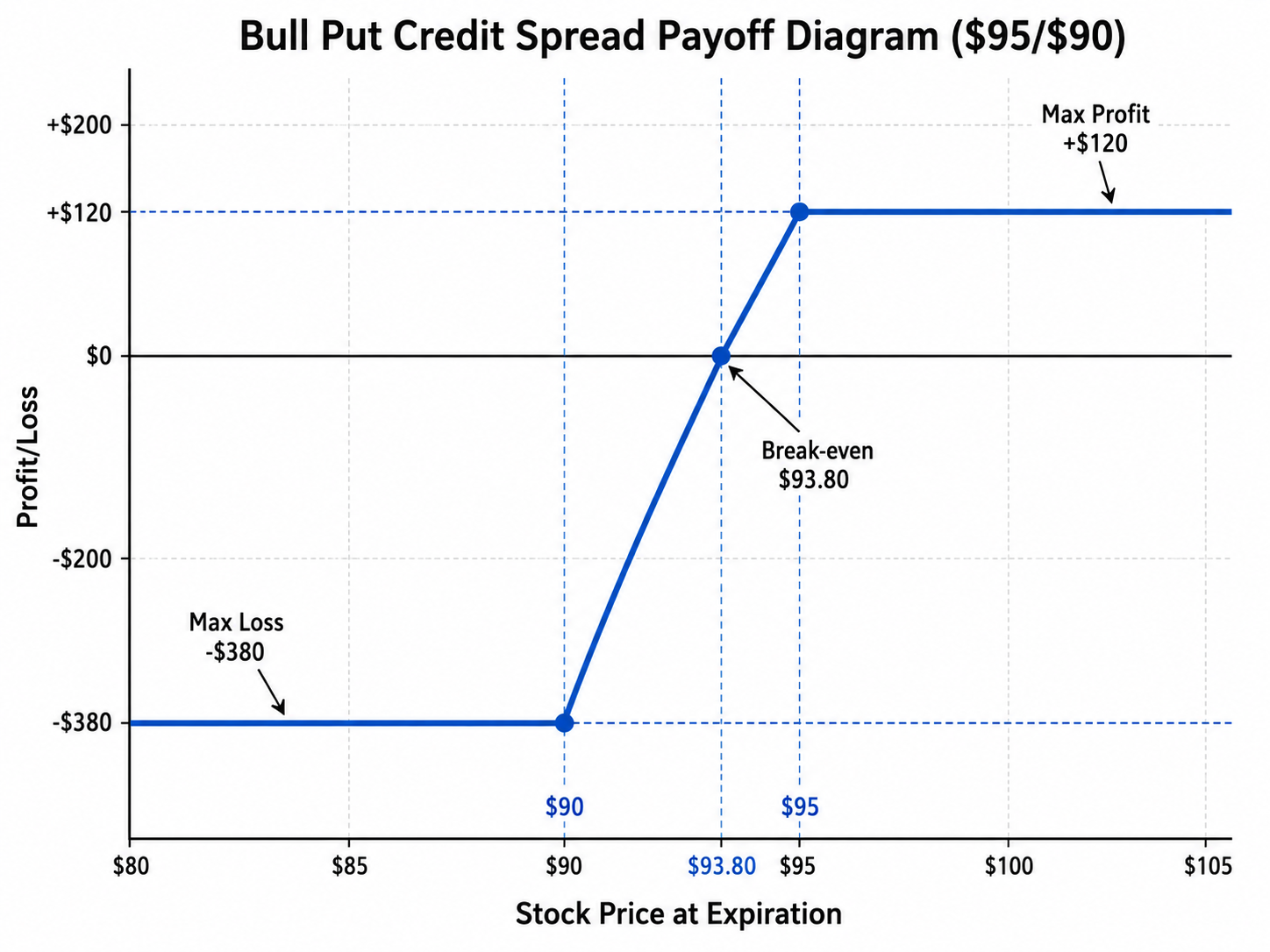

A Concrete Numerical Example of A Credit Spread

Theory tends to click when the dollars are visible. Consider a put credit spread on a fictional stock, XYZ, currently trading at $100, with a mildly bullish outlook over the next 30 days.

The position:

- Sell 1 XYZ $95 put, collecting $1.80 in premium

- Buy 1 XYZ $90 put, paying $0.60 in premium

- Net credit collected: $1.20 per share, or $120 total

- Width of spread: $5, so maximum risk = $500 minus $120 = $380

The most this trade can make is $120. The most it can lose is $380.

Scenario A: The Stock Stays Above $95

Thirty days have passed. XYZ drifts sideways and closes at $98 on expiration day. Both the $95 short put and the $90 long put are out of the money. Both expire worthless. The account keeps the $120 credit collected on day one.

That $120 on $380 of risk works out to roughly a 32% return on capital at risk over 30 days.

Scenario B: The Stock Drops Dramatically

XYZ closes at $87 on expiration day, well below both strikes.

- The $95 put sold is worth $8.00 at expiration (intrinsic value $95 minus $87)

- The $90 put bought is worth $3.00 at expiration (intrinsic value $90 minus $87)

- Net value of the spread: negative $5.00 per share, or negative $500 total

- The $120 credit collected upfront offsets some of that, leaving a realised loss of $380

No matter how far below $90 the stock falls (it could go to $50 or $20), the loss stays capped at $380. The long $90 put stops the bleeding the moment XYZ drops below $90. That cap is the entire reason credit spread options exist as a defined-risk structure. Without the long leg, the position would be exposed to much larger losses as a naked put sale.

The Psychology Behind Credit Spreads

Mechanically, a credit spread is simple. Psychologically, it can quietly trip up unprepared traders.

The first emotional pattern is the asymmetry of the payoff. Risking $380 to make $120 can look like a bad risk reward ratio on the surface. The probability dimension is that the trade is structured so the short strike sits below the current price, meaning the stock has to actually move against the position before the loss kicks in. A well-placed credit spread typically carry a higher probability-of-profit range. Across many trades, the math could work out.

The second pattern is the temptation to hold a losing trade in hope of recovery. With a debit trade paid for upfront, the loss is what was spent on day one, and the cap is automatic. With a credit spread, the loss only crystallises if the stock moves through the short strike. Some traders often watch losses increases, hoping for a reversal, instead of acting on an pre-planed cut loss.

A reframe that often helps: credit spreads are not about being right on direction. They are about being right on a range. That tends to be a more achievable prediction, and is one reason credit spreads scale for traders who treat trading as a process rather than a series of one-off bets.

Common Risks Associated with Credit Spreads

Several risks to consider when applying the strategy.

Risk 1: Defined Loss is Still a Real Loss

The defined-risk feature is helpful, but it can lull beginner options trader into oversizing. A $380 maximum loss on one spread may feel small. Stacking ten of them on the same stock can erase $3,800 on a bad trade. Position sizing tends to be the silent killer of many options trading accounts.

Risk 2: Early Assignment on the Short Leg

If the short option goes deep in the money or has very little extrinsic value left, shares can be assigned (for puts) or called away (for calls) before expiration. With a credit spread, this is rarely catastrophic because the long leg still hedges the position, but it can create a temporary cash crunch, especially in smaller accounts.

Risk 3: Volatility Expansion

Credit spreads tend to profit from falling volatility. When implied volatility spikes, both options gain value, but the short leg tends to gain more (because it carries more vega). A vol spike during a trade window can show a paper loss even if the stock is sitting comfortably between the strikes. Patient traders often ride it out. Reactive traders sometimes close at the worst possible moment.

Risk 4: Pin Risk at Expiration

If the underlying closes exactly at the short strike on expiration day, it is unclear whether the short option will be exercised. The trader may wake up Monday with surprise shares (or surprise short shares) in the account. Many experienced credit spread traders simply close the position earlier either to lock in the profits or cut their losses early before expiration.

Risk 5: Gap Risk

Stocks can gap overnight or over a weekend. Earnings, analyst downgrades, geopolitical events, central bank decisions: any of these can move price past the short strike before the trader has a chance to react. The defined-risk structure caps the dollar loss but cannot prevent a max-loss event from happening in a single morning.

Related Strategies to Explore

Credit spreads sit inside a broader family of premium-selling strategies. The natural next steps for traders exploring this space:

Bull put spread: The bullish flavour of a credit spread, using puts. Tends to profit when the stock stays above the short strike.

Bear call spread: The bearish flavour, using calls. Tends to profit when the stock stays below the short strike.

Cash-secured put: A single-leg options strategy where a put is sold and backed with cash. Higher capital requirement, no long-leg protection, but simpler mechanics.

Covered call: Another premium-selling options strategy, used on shares already owned to generate income but a chance of getting your shares sold.

Traders who enjoy credit spreads often gravitate toward iron condors next. Those who find them intimidating sometimes start with covered calls on stocks they already hold to get comfortable with the income-generation mindset.

Final Thoughts

This guide has covered what a credit spread is, how the two legs interact, the dollar math behind the maximum profit and maximum loss, the psychology many traders confront, and the specific risks that tend to come with the strategy. Many traders treat this material as a starting point for deeper exploration.

Whatever path a trader takes, credit spreads tend to reward patience and punish impulsivity.

This article is for educational purposes only and is not financial advice. Options trading involves substantial risk and is not suitable for every investor/trader.

Frequently Asked Questions

Is a credit spread the same as a vertical spread?

A credit spread is a type of vertical spread, but not every vertical spread is a credit spread. Vertical spreads can also be opened for a debit (debit spreads), where net premium is paid upfront because the option bought costs more than the option sold.

Can a credit spread lose more than the credit received?

Yes. The credit is the maximum profit. Maximum loss is the width of the spread minus the credit, multiplied by 100. Both numbers are knowable at trade entry.

Why do credit spreads pay so little compared to single options?

Because they trade probability for size. The trader collects a smaller premium in exchange for a higher likelihood of winning. Over many trades, more frequent small wins can compound faster than infrequent large wins, provided losses are managed.

Does trading credit spreads require a margin account?

At most brokers, yes. Credit spreads are defined-risk, so they typically require less buying power than naked options, but a brokerage account approved for spread trading is generally needed (often level 3 options approval at retail brokers).

submit your comment