Both debit and credit spread options strategy structures share the same strike prices, the same expiration, the same underlying. Yet they behave differently depending on time decay, implied volatility, and the speed of the move. Some option traders that trade spreads for the first time might wonder why they could be directionally right, yet the options trade still loses money.

This guide breaks down the credit spread vs debit spread comparison into a framework readers can apply. It covers the mechanics, the Greeks, the breakeven math, the volatility profiles, and the psychological patterns of each.

What Are Credit Spreads and Debit Spreads?

Both belong to a broader family called vertical spreads. A vertical spread is two options of the same type (calls or puts), same expiration, but different strikes, bought and sold simultaneously.

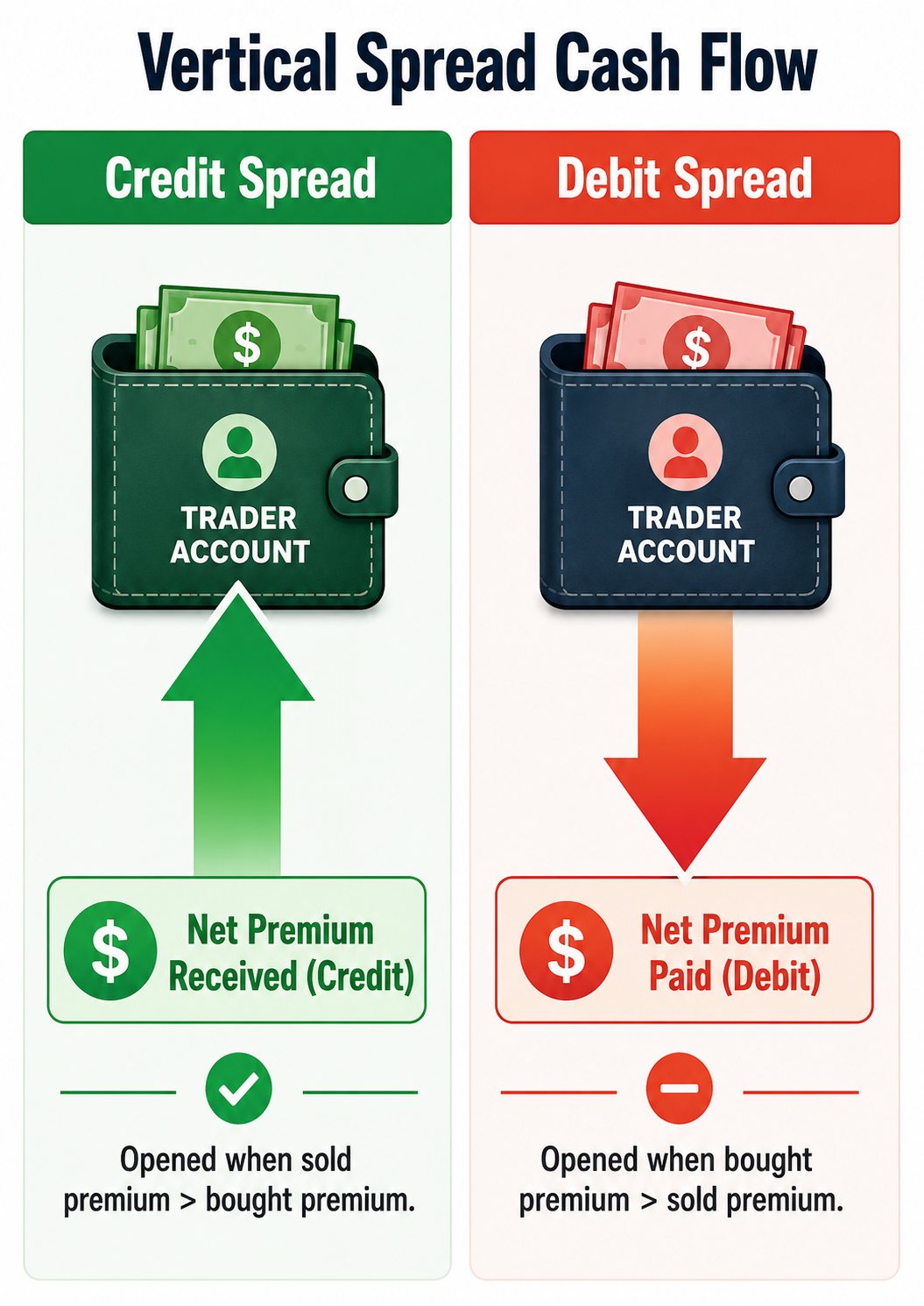

A credit spread consists of two options contracts, where the option sold carries a higher premium than the option bought. Net cash flows into the account on day one, the trader receives a credit. That's why it's called a credit spread.

A debit spread is the reverse: the option bought carries a higher premium than the option sold. Net cash flows out of the account on day one, the trader pays a debit. That's why it's called a debit spread.

Two structures, same toolbox, opposite philosophy. Which one works better comes down to the trader's setup and the market environment.

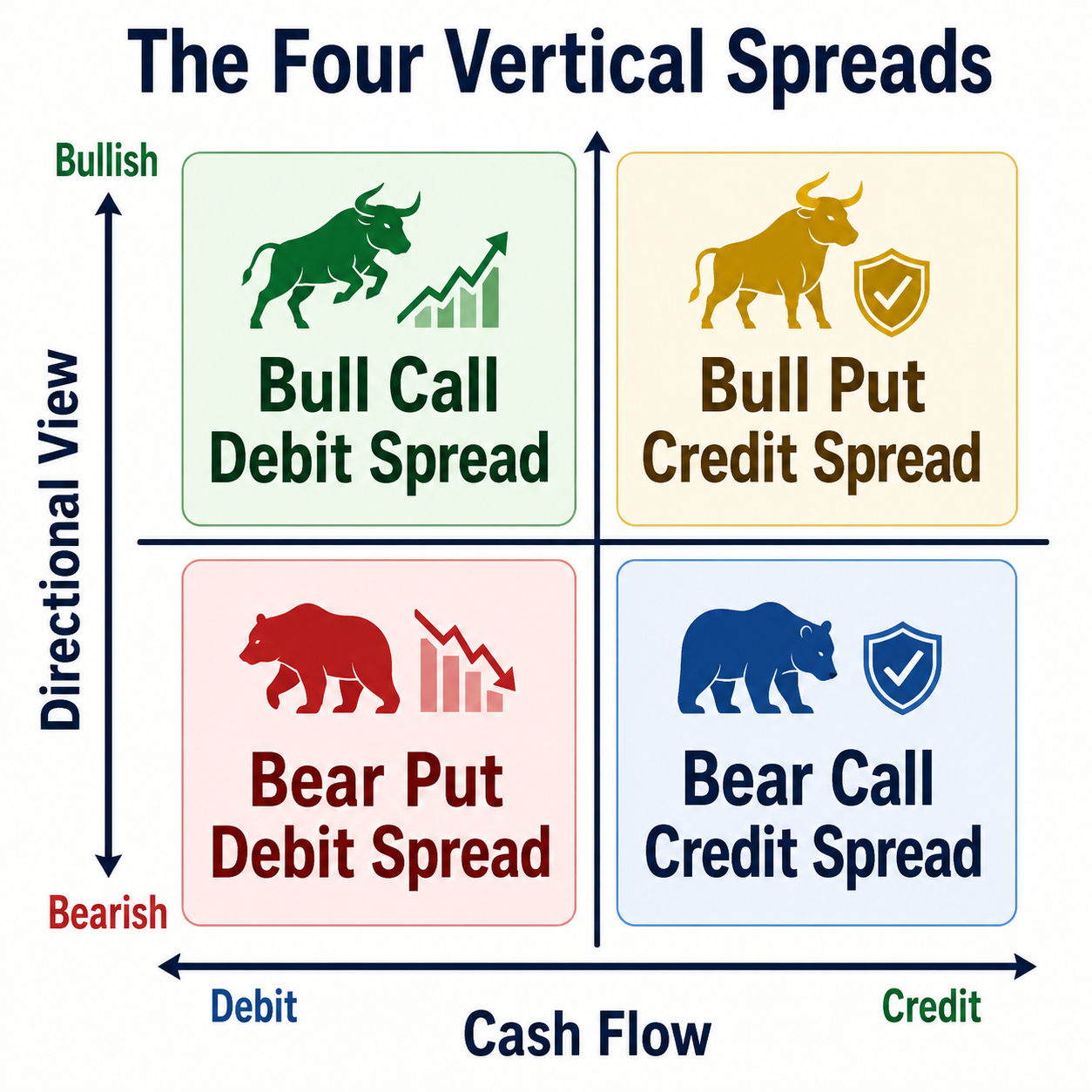

How the Four Vertical Spreads Map

Between Debit and Credit spread, there are 4 basic strategies:

1. Bull put credit spread (bullish, credit)

2. Bear call credit spread (bearish, credit)

3. Bull call debit spread (bullish, debit)

4. Bear put debit spread (bearish, debit)

The Core Mechanical Difference

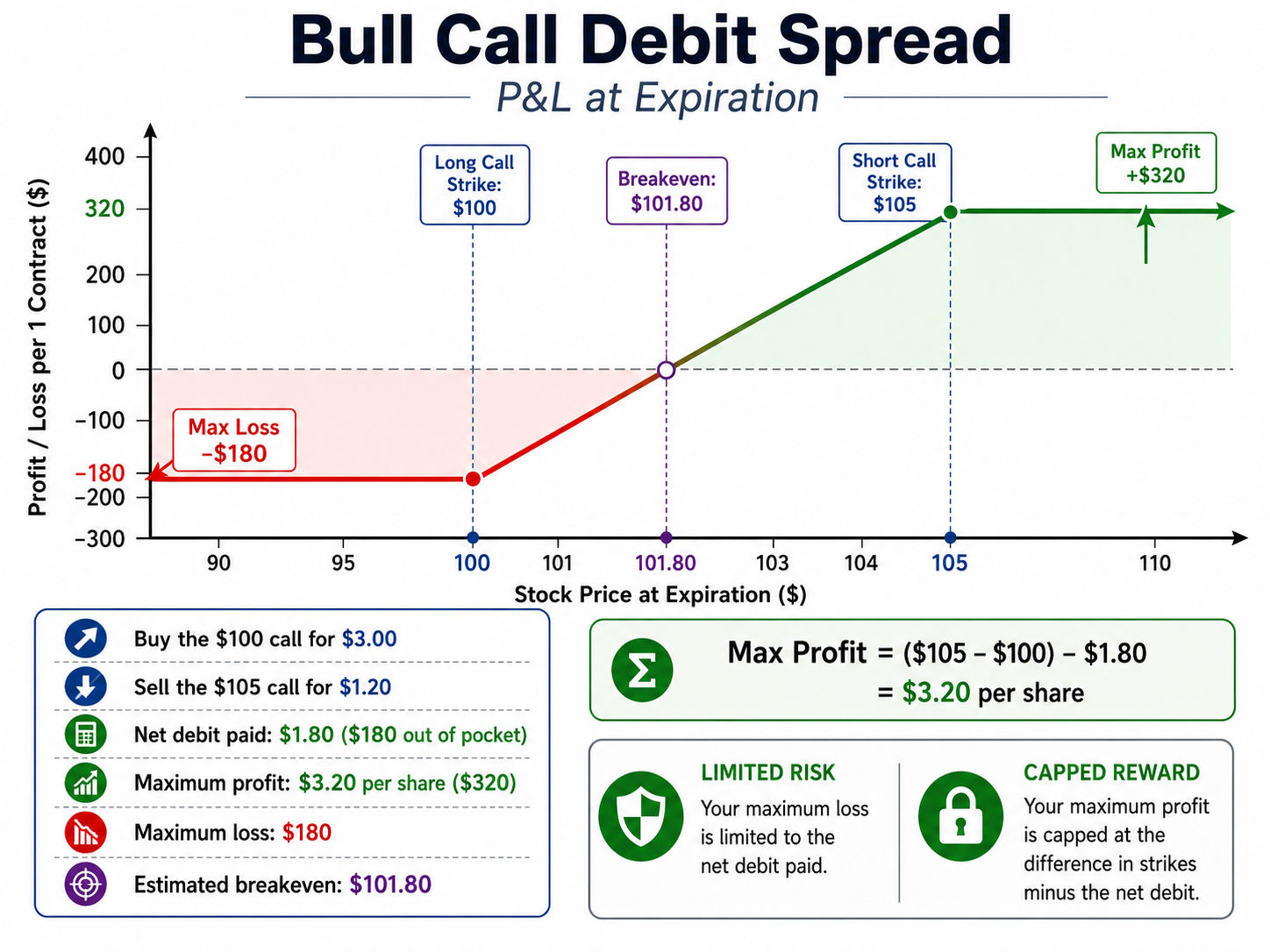

To anchor the difference, consider stock XYZ trading at $100. The view is mildly bullish over the next 30 days.

This view can be expressed with the 2 following bullish strategies.

A Bull Call Debit Spread

- Buy the $100 call for $3.00

- Sell the $105 call for $1.20

- Net debit paid: $1.80 (so $180 out of pocket)

- Maximum profit: ($105 minus $100) minus $1.80 = $3.20 per share, or $320

- Maximum loss: $180 (the debit paid)

- Estimated Breakeven: $101.80 (lower strike plus debit)

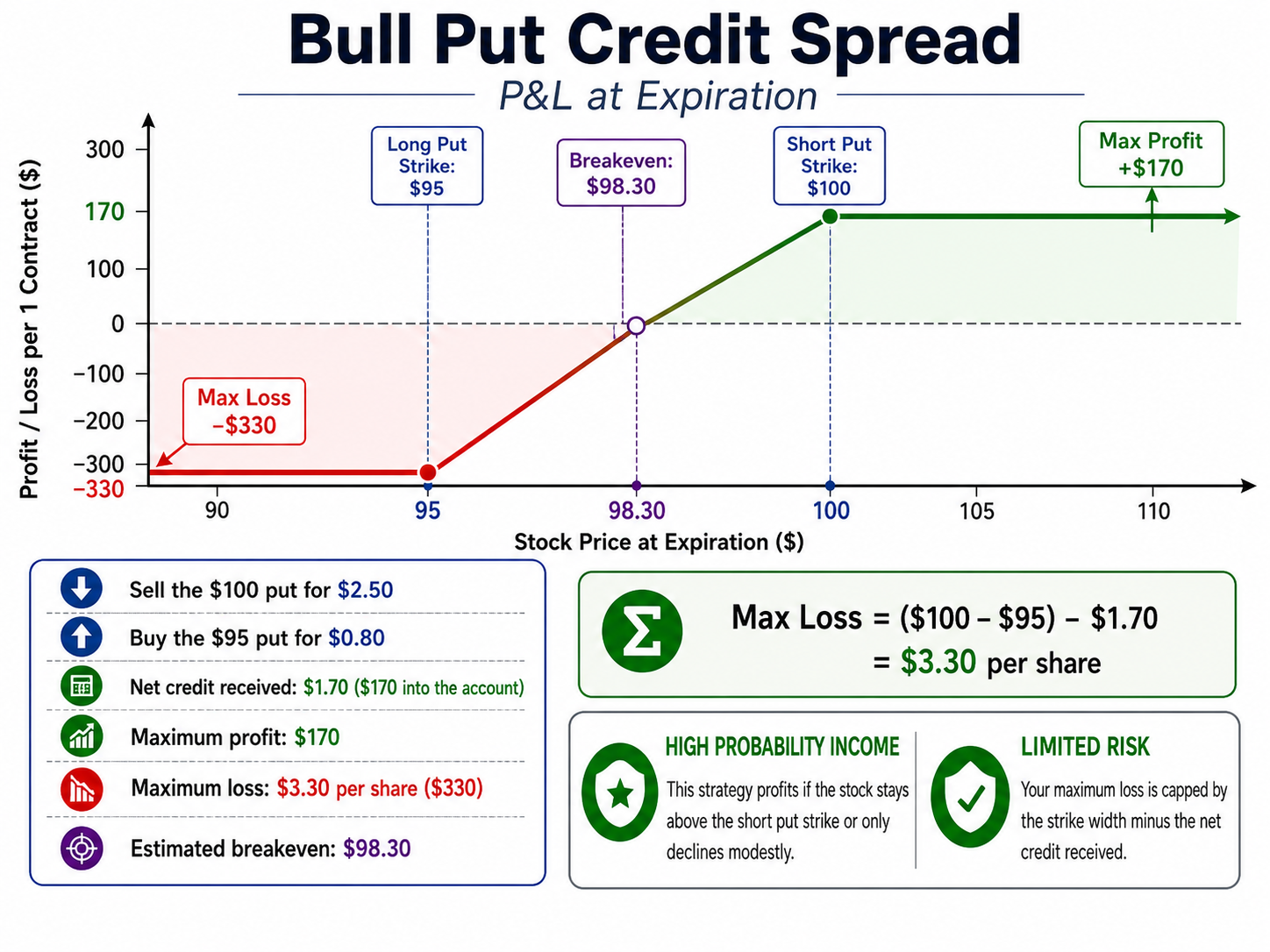

A Bull Put Credit Spread

- Sell the $100 put for $2.50

- Buy the $95 put for $0.80

- Net credit received: $1.70 (so $170 into the account)

- Maximum profit: $170 (the credit)

- Maximum loss: ($100 minus $95) minus $1.70 = $3.30 per share, or $330

- Estimated Breakeven: $98.30 (short strike minus credit)

Same underlying. Same bullish view. Same 30-day window. Different cash flow, different breakeven, different P&L profile. The credit vs debit spread choice changes how much is risked, how much can be earned, and what the stock needs to do for the trade to win.

How Time Decay Affects Each Spread

A debit spread is a position, where you pay a premium. The option bought has more time value than the option sold. Which means that every day that passes, the net position loses extrinsic value. The trader is fighting the clock. If the stock sits still, the debit spread can quietly bleed out, even when the directional view is eventually proven correct.

A credit spread is a position where you are paid a premium on day one. The option sold has more time value than the option bought. Every day that passes, the net position gains. Sideways action can be a friend. Even if the stock barely budges, time decay slowly converts your position into profit.

This mechanic is why credit spread vs debit spread options behave differently. Two traders with the same directional view, taking opposite spread structures, can experience opposite outcomes.

Debit spreads are often associated with expected moves; credit spreads are often associated with expected pauses or range-bound conditions.

How Implied Volatility Affects Each Side

The other consideration of the call credit spread vs call debit spread decision is implied volatility (IV).

When IV expands on a debit spread, the long option tends to gain more value. Overall rising IV tends to help. Falling IV tends to hurt.

When IV expands on a credit spread, the short option tends to gain more value. Overall rising IV tends to hurt. Falling IV tends to help.

A trader aware of these dynamics can take a benchmark approach to volatility. Higher IV environments are sometimes associated with better credit spread setups and when IV is lower, debit spreads tend to have better setups. The reason is simple, elevated IV offers richer premiums to collect, while compressed IV means paying less for a long premium with room for expansion.

Probability vs Payoff of Both Spreads

A credit spread and a debit spread compared at the same width and strikes tend to show this pattern:

The credit spread has lower maximum profit with a higher probability of profit

The debit spread has higher maximum profit with a lower probability of profit

Options markets are reasonably and logically efficient. High probability and high reward in the same package tend not to coexist. So the credit spread vs debit spread options decision is less about which is "better" and more about which trade-offs fit the situation.

Worked Example: Same View, Two Structures, Two Outcomes

To push the example further, XYZ remains at $100, with a bullish 30-day view.

Three real-world scenarios:

The two trades being compared:

Bull call debit spread: long $100 call, short $105 call, paid $1.80 debit (risk $180, max profit $320)

Bull put credit spread: short $100 put, long $95 put, collected $1.70 credit (risk $330, max profit $170)

Scenario 1: Stock Rips Higher to $108 by Expiration

Debit spread: full max profit, $320 gained

Credit spread: full max profit, $170 gained

Both win. The debit spread wins bigger. This is the case the debit spread is typically structured for.

Scenario 2: Stock Drifts Sideways and Closes at $100.50

Debit spread: at expiration, the $100 call is worth $0.50, the $105 call is worthless. The spread settles at $0.50, resulting in a loss of $130 (paid $1.80, recovered $0.50)

Credit spread: at expiration, the $100 put is barely worth anything; the $95 put is worth $0. Both expire effectively worthless. The full $170 credit is kept.

Same direction, almost no movement. The debit spread loses. The credit spread wins. This is a common outcome that rewards credit spread sellers.

Scenario 3: Stock Drops to $94 by Expiration

Debit spread: both calls expire worthless. The full $180 paid is lost.

Credit spread: both puts are in the money by $6 and $1 respectively. The spread settles at $5.00. The $1.70 credit collected is offset by the $5.00 close cost, resulting in a $330 loss.

Both lose. The credit spread loses more here because the width was $5 and the original credit was small relative to the move.

These three scenarios illustrate why a directional view alone tends not to be enough. The speed and magnitude of the expected move usually matter just as much. Together, they give traders a glimpse into the efficiency of options trading: the ability to structure a position around almost any market outlook, as long as the trader is clear on what outcome they're aiming for.

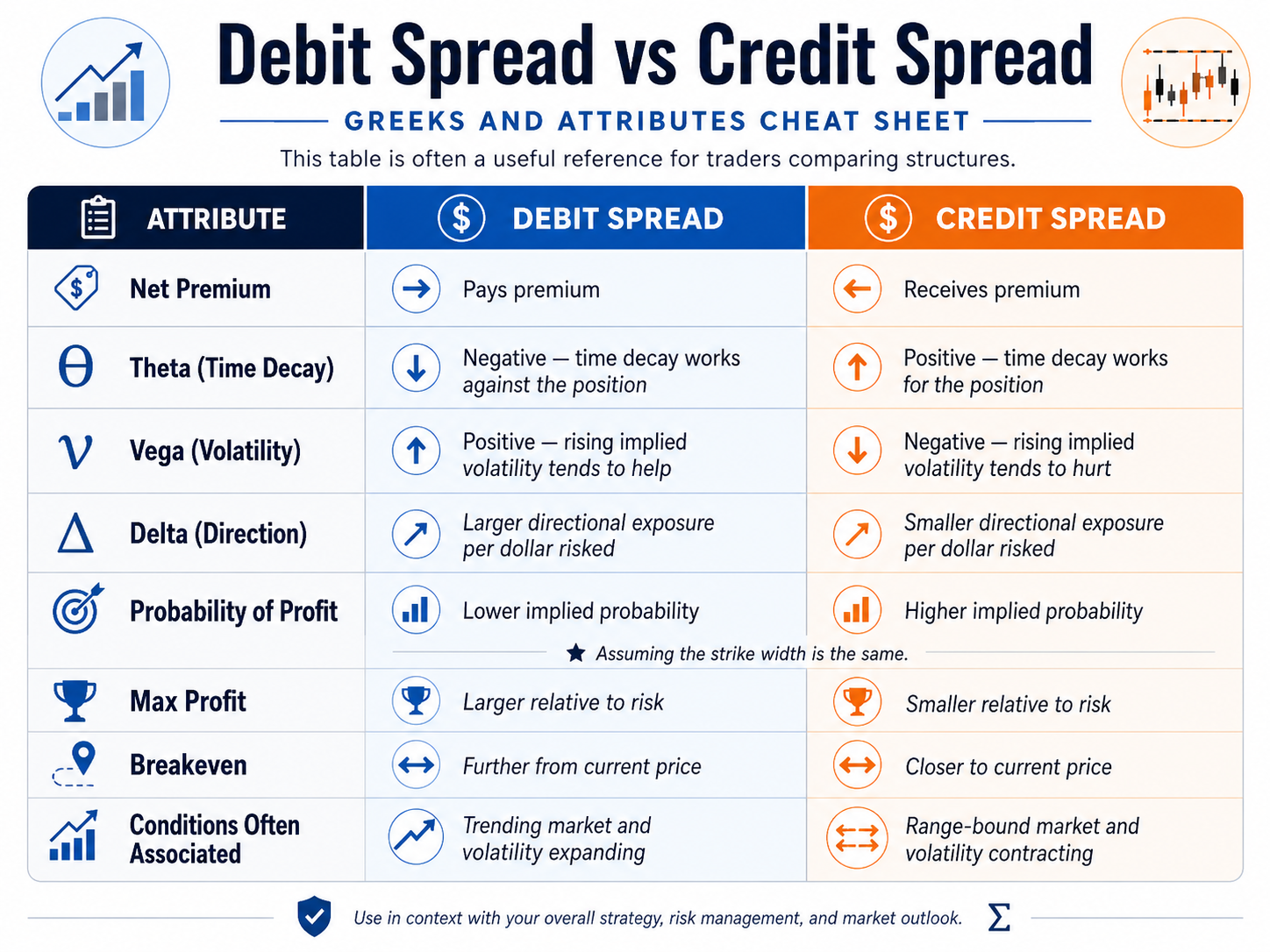

Greeks Summary: Credit Spread vs Debit Spread

A cheat sheet for the credit debit spread comparison from a Greeks perspective:

The Psychology Around Credit and Debit Spreads

Traders tend to judge a strategy as "good" or "bad" based on risk-reward alone and that instinct works against both credit and debit spread traders in different ways.

The credit spread trader has to absorb the emotional weight of an asymmetric payoff: collecting $1.70 while risking $3.30 feels backwards, even when the math favors them. Every max-loss can trigger a sense that the strategy is broken, even though the implied probability of winning tends to be higher.

The common pitfall is panicking after the first painful loss and abandoning the system.

The debit spread trader has to absorb the slow grind of decaying premium. Theta is invisible but relentless, the position can drift red even when the chart isn't doing anything. This often leads to unnecessary action: rolling, closing too soon, or on the flip side, letting a losing trade compound because "the stock is so close to my breakeven."

A reframe many traders find useful: the goal is never to predict the future, but to take a structured bet on a probability distribution. Credit spreads tilt that distribution toward a high-probability, low-payout outcome. Debit spreads tilt it toward a low-probability, high-payout outcome. Neither is universally correct, they're tools matched to different situations.

Risks Specific To Each Structure

Risks Often Associated with Credit Spreads

Loss size: Per trade, the loss can exceed the gain. Position sizing matters.

Tail-risk events: Gaps and earnings surprises can blow through the short strike. Some traders even completely avoid catalyst events like earnings in their options trading.

Discipline: With a close breakeven, it can be tempting to hold losing trades. Many traders set rules in advance.

Risks Often Associated with Debit Spreads

1. Time decay: Theta erodes value when nothing happens. A correct directional view at the wrong speed can still lose.

2. Volatility crush: Buying spreads ahead of earnings when IV is rich is a classic example of how volatility crush works against the trader. Even if direction is right, IV collapse can offset the move and cut profits.

3. Path matters: A debit spread that touches profit but does not stay there until expiration can give back gains.

4. Lower win rate: Losses are more frequent, which can be psychologically draining if traders are not expecting it.

Related Strategies to Explore

Once the debit vs credit spread options comparison feels intuitive, the next layers of options strategy tend to open up:

Iron condor: Combine a bear call credit spread and a bull put credit spread to profit from a range.

Iron butterfly: A tighter, more aggressive cousin of the iron condor.

Calendar spread: Mixes expiration cycles to play on time decay differences.

Diagonal spread: A debit-or-credit hybrid that lets a trader hold longer-dated long options against shorter-dated short options.

Ratio spreads: For combinations where a credit and a directional payoff are layered together.

Final Thoughts

The credit spread vs debit spread decision is less about which strategy is superior and more about matching the structure to the market environment, the directional view, the volatility regime, and the trader's psychology. The edge in options trader comes in choosing the right strategy for the right environment.

The cheat-sheet table above, the worked example, and the conditions associated with each structure form a useful reference. Many traders practise both structures on paper to watch how they behave through time decay, IV moves, and surprise gaps.

This article is for educational purposes only and is not financial advice. Options trading involves substantial risk and is not suitable for every investor.

Frequently Asked Questions

Is a credit spread or debit spread better?

Neither is universally better. Credit spreads tend to perform in high-IV, sideways markets. Debit spreads tend to perform in low-IV, trending markets. The fit depends on the current environment.

Can a credit spread lose more than a debit spread?

Yes, if the widths are equal. A 5-point credit spread that collected $1.70 can lose $3.30 per share. A 5-point debit spread that paid $1.80 can only lose $1.80 per share.

Is a call credit spread the same as a put debit spread?

Both are bearish, but they have different cash flows, breakevens, and Greek profiles. A call credit spread is bearish and short premium. A put debit spread is bearish and long premium. The fit between them often depends on IV, time horizon, and how aggressive the directional bet is.

Which is easier for beginners, debit or credit spreads?

Mechanically, debit spreads tend to be simpler because the max loss equals what was paid. Credit spreads can suit beginners psychologically because the higher win rate builds confidence. Many traders learn both, starting on paper or with single contracts.

Can a credit spread be converted into a debit spread mid-trade?

Rolling or restructuring is possible, yes. It usually means closing one and opening the other, which incurs commissions and slippage. Picking the appropriate structure upfront tends to be cleaner than restructuring later. Especially when tabulating the profit and loss from the trades.

submit your comment