Everyone is talking about the SpaceX IPO right now. And we get it. This is one of those rare financial moments that feels genuinely historic.

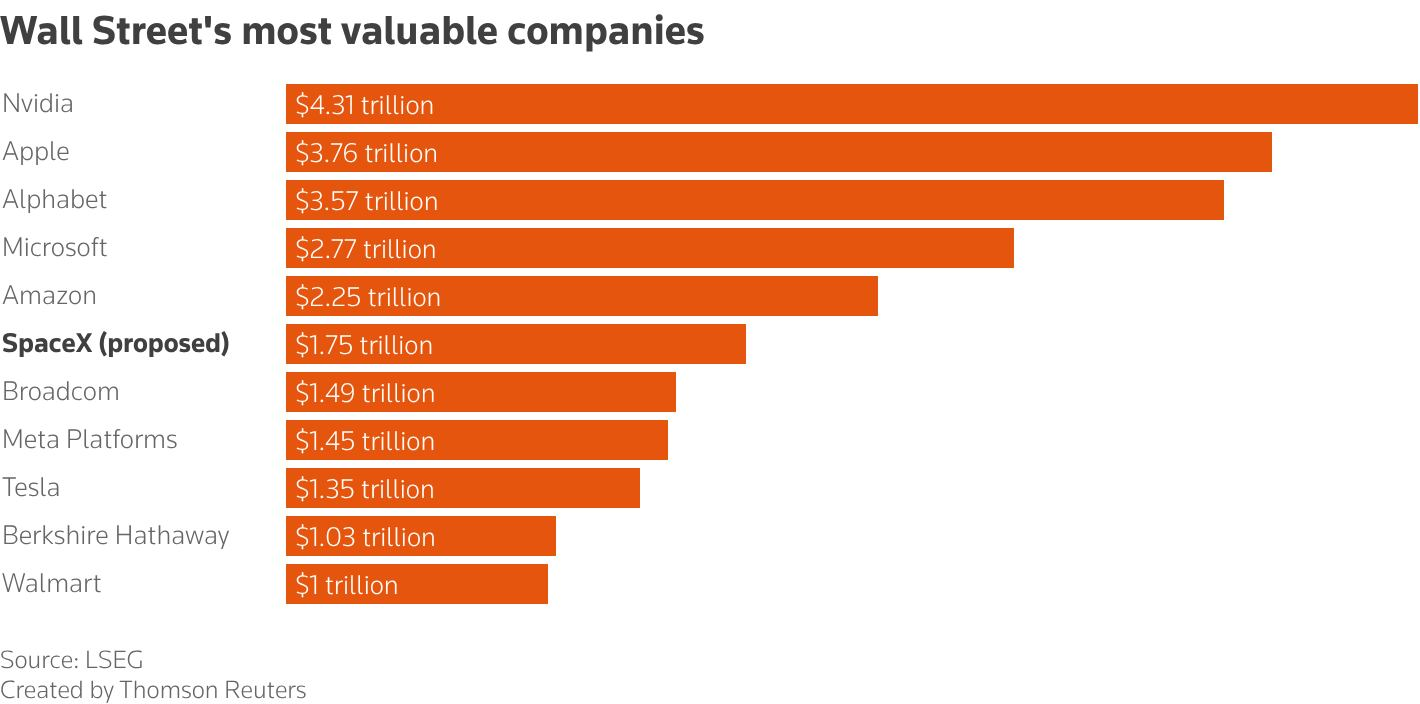

SpaceX has confidentially filed its S-1 with the SEC. And Bloomberg reports that the valuation target has climbed above $2 trillion, up from $1.75 trillion just two weeks ago and $1.25 trillion when the xAI merger closed in February. If it goes through, this will be the largest IPO in the history of capital markets, potentially raising up to $75 billion, nearly triple of Saudi Aramco's $25.6 billion record back in 2019.

In a meeting with the full bank syndicate on Monday night, SpaceX CFO Bret Johnsen confirmed that the company will allocate an unprecedented portion of shares to retail investors, reportedly up to 30%, three times the typical norm.

His exact words, according to Reuters: "Retail is going to be a critical part of this and a bigger part than any IPO in history. Those are folks that have been incredibly supportive of us and of Elon for a long time, and we want to make sure that we recognise that."

Now, we want to be clear. SpaceX is a phenomenal business. It has genuinely revolutionised space launch, built a global broadband constellation from zero to 10 million subscribers in under five years, and generated real, growing revenue in the process. The main issue is with the price. And at $2 trillion, the math is challenging.

The AI bubble won't pop quietly. Find out where to be before it does. →

The Valuation Math of the expected SpaceX IPO

There is a famous quote that every investor needs to hear before buying this IPO, and it comes from Scott McNealy, the co-founder of Sun Microsystems.

Sun was one of the biggest darlings of the dot-com bubble. At its peak, the stock traded at 10 times revenue. After it collapsed from $64 to under $10, McNealy said this in a 2002 Bloomberg interview:

"At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are?"

McNealy was talking about 10 times sales. Sun eventually got acquired by Oracle for $7.4 billion, a drop of more than 95% from its peak market cap of $200 billion.

Now here is the math on SpaceX.

According to Reuters, SpaceX generated approximately $15 to $16 billion in revenue and roughly $8 billion in profit in 2025 on its rocket and Starlink business. After the xAI merger, Bloomberg analysts expect combined revenue to approach $20 billion in 2026, with xAI contributing less than $1 billion of that.

At a $2 trillion valuation:

- Price-to-Sales (2025 revenue): approximately 125x

- Price-to-Sales (2026E revenue): approximately 100x

- Price-to-Earnings (2025 profit): approximately 250x

At 100 times sales, you need the company to hand you 100% of revenue for 100 years, assuming zero costs, zero taxes, zero R&D, zero satellite replacement, and zero competition, just to get your money back.

And remember, this is not a software company with 80% gross margins and near-zero marginal costs. SpaceX builds rockets. It launches satellites. It must continuously refresh a constellation of thousands of satellites in orbit. The capital intensity profile is closer to a telecom or an airline than to a SaaS business.

Satellite industry analyst Armand Musey put it directly: "SpaceX is the most anticipated IPO in history. However, there are lots of questions about valuation and how the current company can justify the price talk. It can't. At the end of the day, the IPO pricing is a bet on Elon Musk's and his team's ability to deliver new products and services that either don't exist or that we might not even foresee."

The xAI Problem Nobody Is Talking About

When you buy SpaceX at IPO, you are not just buying Starlink and rockets. You are buying a combined entity that now includes xAI (Musk's AI venture) and X (the social media platform formerly known as Twitter). The February 2026 all-stock merger valued SpaceX at $1 trillion and xAI at $250 billion, for a combined $1.25 trillion.

The problem is that xAI is haemorrhaging cash. Reports indicate xAI generated approximately $250 million in revenue over six months while losing $2.5 billion.

The IPO will also feature a dual-class share structure giving Musk outsized voting control. So to summarise what you are actually buying at $2 trillion: a genuinely dominant launch and broadband business, stapled to a cash-incinerating AI lab, a social media platform with regulatory issues across multiple jurisdictions, and a governance structure that gives you no meaningful say in how capital gets allocated between any of them.

Starlink Is Extraordinary, but does it make it a good investment?

Let’s talk about Starlink.

Starlink crossed 10 million subscribers by February 2026. The growth curve has been stunning: 1 million in December 2022, 4 million by September 2024, 9 million by December 2025, and 10 million by February 2026, adding the last million in just 53 days.

Starlink generated roughly $10 billion in revenue in 2025 and now represents the core revenue engine of SpaceX. The constellation consists of over 10,000 active satellites, comprising 65% of all active satellites in orbit, and accounts for 97.1% of all global satellite broadband Speedtest samples according to Ookla data.

But even the most optimistic Starlink scenario requires subscriber counts in the hundreds of millions, sustained average revenue per user, and a continuous satellite replacement cycle that must be funded at massive scale, all while Amazon, Eutelsat OneWeb, Telesat, and Chinese state-backed constellations ramp up to compete. Getting from $10 billion to the $80 to $100 billion in revenue that would begin to justify a $2 trillion market cap is a decade-long journey through real competition and enormous capital requirements.

Alternative #1: Amazon, the Most Dangerous Starlink Competitor at a Fraction of the Price

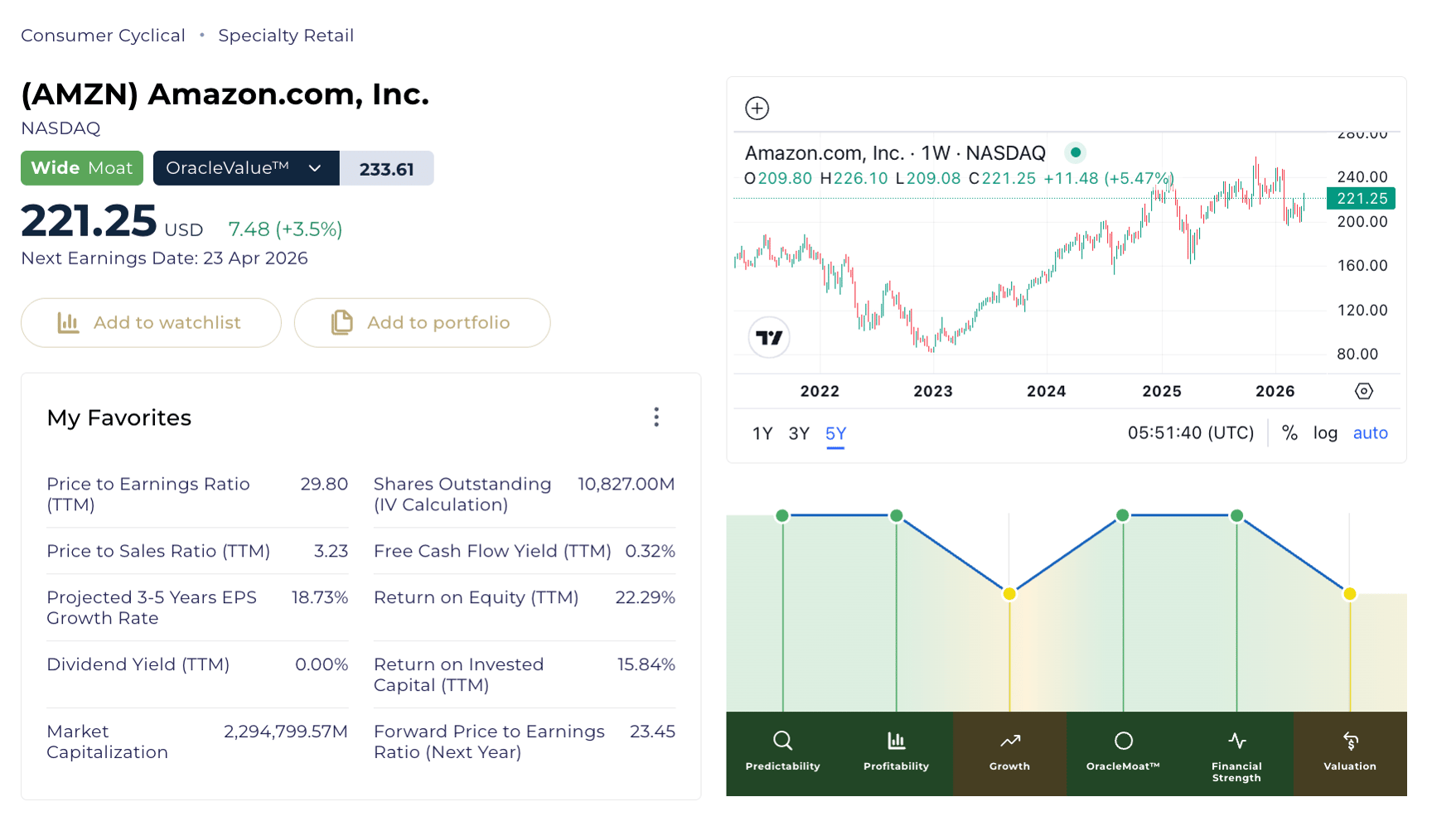

Here is how investors can invest in Space instead of rushing into SpaceX IPO: they can get significant exposure to the space economy through Amazon at a dramatically more attractive valuation, while also owning the world's largest cloud platform, a dominant e-commerce franchise, and a rapidly growing advertising business.

Amazon StockOracle™ First Load Dashboard Accurate as of 09 Apr 2026

Amazon trades at roughly $220 per share with a market cap of approximately $2.29 trillion, a trailing P/E of around 29, a forward P/E of roughly 24, and a price-to-sales ratio of 3.23.

Amazon Leo (formerly Project Kuiper) is the most credible Starlink competitor in the world. Amazon has completed nine launch missions and deployed 241 production satellites. The company plans 20 more launches in 2026 and over 30 in 2027, and expects to have 700 satellites in orbit by mid-2026.

What makes Amazon Leo uniquely dangerous to SpaceX is the AWS integration moat. Amazon can bundle satellite connectivity with AWS cloud services, security, and device management from a single vendor. Industry analysts expect Amazon to bundle Leo with Prime memberships and AWS cloud services, replicating the same bundling playbook that made AWS dominant in cloud computing.

Wall Street values Amazon on AWS growth, e-commerce margins, and advertising. Leo is still treated as a cost centre. If Amazon Leo achieves even $15 to $20 billion in annual revenue at high margins within five to seven years, valued at a conservative 8 to 10x revenue, that is $120 to $200 billion in incremental enterprise value, or roughly $11 to $19 per share of additional value not reflected in today's price.

With SpaceX, you are paying 100 to 125 times sales for space exposure. With Amazon, you are getting it as an unpriced call option at 3 times sales, wrapped inside the world's best e-commerce, cloud, and advertising flywheel.

Alternative #2: Alphabet, a $110 Billion SpaceX Stake You Can Buy at 27x Earnings

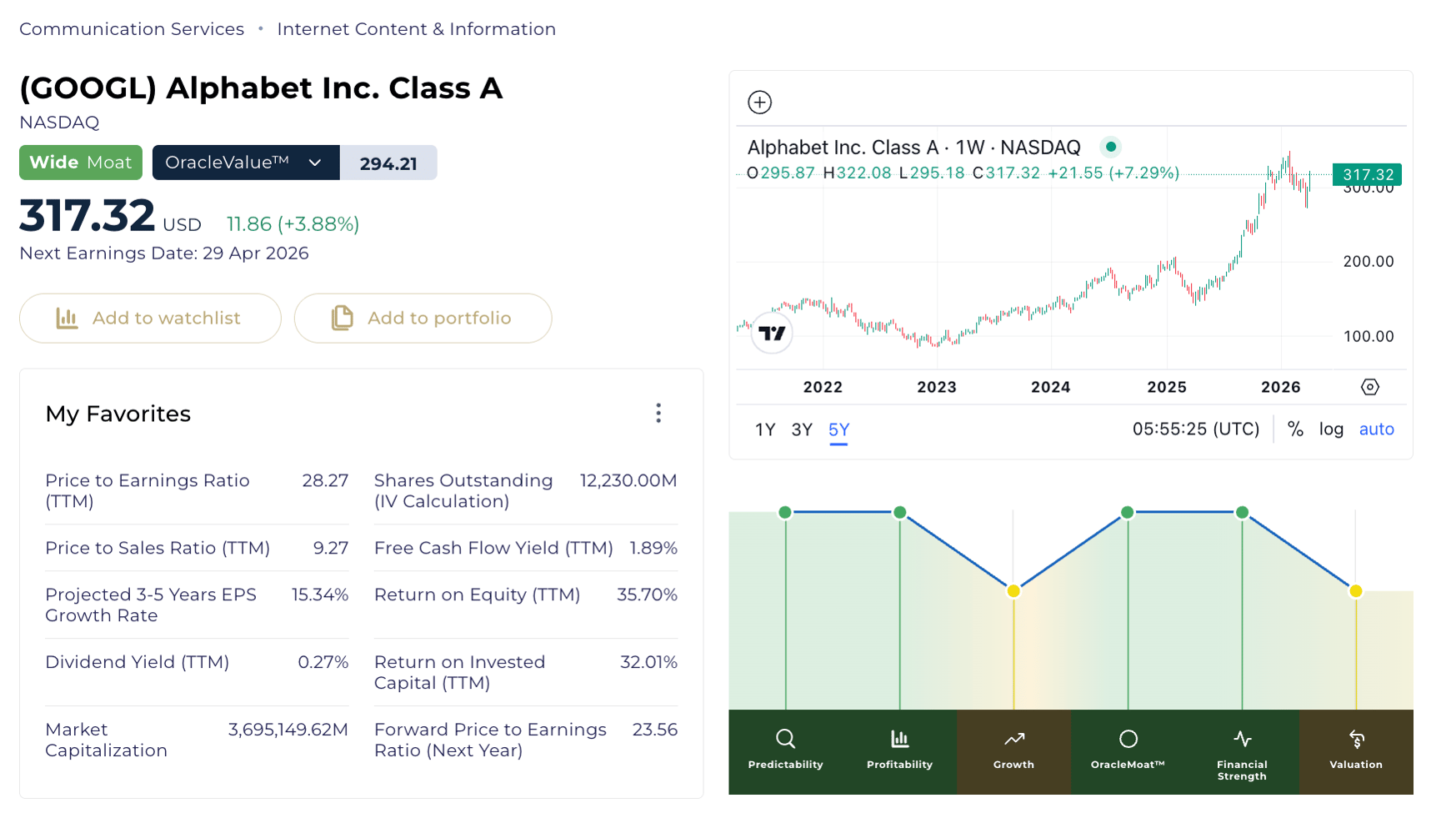

For investors who specifically want direct exposure to SpaceX itself, there is an elegant backdoor that most people overlook when thinking about investing in Space: Alphabet.

In 2015, Alphabet invested roughly $900 million to acquire what is now estimated at a 7% stake in SpaceX, when the company was valued at approximately $12 billion.

If SpaceX IPOs anywhere near $1.5 to $2 trillion, that stake becomes worth $110 to $140 billion. It would instantly rank as one of the most successful venture capital bets in modern history.

In Q1 2025, Alphabet disclosed approximately $8 billion in unrealized gains tied to its SpaceX holding.

Google StockOracle™ First Load Dashboard Accurate as of 09 Apr 2026

Alphabet currently trades at roughly $317 with a market cap of approximately $3.68 trillion and a P/E of about 28. The SpaceX stake represents roughly 3 to 4% of Alphabet's market cap. When SpaceX IPOs, that stake gets publicly marked to market for the first time, creating a clear catalyst for re-rating because it crystallises a hidden asset that has been buried in the financial statements under "non-marketable equity securities."

Beyond SpaceX, Alphabet also holds a roughly 10% stake in AST SpaceMobile, has investments in Planet Labs, and is developing Project Suncatcher, its own orbital data centre initiative with prototype satellite launches planned for 2027.

Alternative #3: Space ETFs, broad space exposure

ARKX (ARK Space & Defence Innovation ETF) is actively managed with a 0.75% expense ratio. Top holdings include L3Harris, Kratos, and Rocket Lab. It returned approximately 74% over the past year.

UFO (Procure Space ETF) offers broader exposure with roughly 50 holdings, though its 0.94% expense ratio is high and the portfolio tilts toward higher-risk small-caps.

ROKT (SPDR S&P Kensho Final Frontiers ETF) is passively managed with a lower 0.45% expense ratio and skews toward defence and industrial names with space exposure, making it the lower-volatility option.

The Bottom Line

The space economy is real. The global space economy reached $626 billion in 2025, with 321 successful orbital launches and private investment recovering to $9 billion. McKinsey and the World Economic Forum project the sector reaching $1.8 trillion by 2035.

But great companies and great investments are not always the same thing. The price you pay determines your return, and that is true regardless of how extraordinary the underlying business is. At $2 trillion, SpaceX's IPO demands that virtually everything goes right for a very long time before shareholders see a meaningful return.

If SpaceX comes public and the S-1 reveals a financial picture that is materially better than what current estimates suggest, that changes the calculus. But as it stands today, with the information available, the risk-reward across other parts of the space economy looks considerably more attractive.

This article is for educational purposes only and does not constitute investment advice. All investors should conduct their own due diligence before making investment decisions.

submit your comment